AR Is a Sales Problem, Not Just a Finance Problem

Every sales team tracks CAC, pipeline, and close rate. Almost none of them track what happens to payment behavior after the contract is signed. That disconnect is costing businesses more than they realize, and it starts with a structural misunderstanding of where AR actually sits in the revenue cycle.

Sia Ghazvinian

Co-Founder & CEO

Table of contents

Share

There is a moment in almost every B2B business where the handoff goes wrong. Sales closes the deal, passes the account to finance or operations, and moves on to the next opportunity. The invoice goes out. The clock starts. And the relationship that took months to build gets handed to a process that was designed for the back office, not for the customer.

This handoff is where accounts receivable stops being treated as part of revenue generation and starts being treated as an administrative function. That reframing is costly. And it is structurally wrong.

AR is not the end of the revenue cycle. It is the last mile of it. How that last mile is executed determines not just whether you get paid, but whether the customer pays again, and whether they ever refer anyone else to you.

The Organizational Blind Spot

Ask most sales leaders what happens after a deal closes and you will get a version of the same answer: that is a finance problem. Ask most finance leaders what drives late payment behavior and you will get a version of this: customers just pay late sometimes.

Both answers are partially true. Neither is strategically useful.

The organizational structure of most B2B companies reinforces this blind spot. Marketing owns acquisition. Sales owns pipeline and close. Customer success owns onboarding and retention, sometimes. Finance owns billing and collections. These functions often have separate leadership, separate metrics, and separate priorities. Nobody owns the full arc from first contact to final payment.

The result is a gap. Payment behavior data sits in finance systems. Relationship data sits in the CRM. Neither team is reading the other's signals. And when a client starts paying late, which, according to PYMNTS research, is one of the earliest and most reliable predictors of churn, neither team is positioned to act on it in time.

Payment Behavior Is Customer Health Data

This is the insight that most businesses are sitting on without realizing it. Payment behavior is not just a financial metric. It is behavioral data about your customer relationship.

A client who has paid on time for 18 months and suddenly goes 30 days overdue is telling you something. Maybe their business is under cash pressure. Maybe there is internal friction in their AP process. Maybe they are dissatisfied with a recent delivery and using payment as a passive form of dispute. Maybe a key contact who championed your relationship has left the company, and research shows that accounts lose up to 25% more to churn risk when a key internal contact departs.

Any of these signals matters to your sales and customer success teams. None of them will see it if AR data lives in a silo that finance manages alone.

According to PYMNTS' 2025 analysis of B2B payments data and retention, machine learning models built on payment behavior history can detect churn signals that traditional relationship management systems miss entirely, particularly changes in payment frequency, method, and timing. The data already exists. Most businesses simply are not using it.

The Cost of Treating AR as a Back-Office Function

The financial case for changing this is straightforward. Retaining an existing customer costs a fraction of acquiring a new one, the widely cited ratio is five times cheaper, and in enterprise B2B the gap is even larger. A 5% improvement in customer retention can increase business profitability by up to 95%, according to research modeled across B2B contexts.

When AR is managed in isolation from the customer relationship, it introduces friction at a sensitive moment in the client lifecycle. A collections sequence that is tonally aggressive, poorly timed, or disconnected from the broader relationship context does not just risk non-payment. It risks the entire account.

The 2025 data on involuntary churn makes this concrete. Up to 40% of total B2B churn stems from payment failures and billing friction, not from product dissatisfaction or competitor switching. These are not customers who wanted to leave. They were lost to a process failure. And early detection of payment issues, combined with proactive recovery, can reduce this involuntary churn by 25 to 40%.

That is retention improvement available to any business that connects its AR process to its customer success function. Most businesses are not making that connection.

Where Sales Creates AR Problems Downstream

The sales function contributes to AR outcomes in ways that rarely get examined honestly. Three patterns show up consistently:

• Payment terms negotiated in the deal. When sales teams have discretion over payment terms and use that discretion to close deals faster, extending net 60 or net 90 terms without finance alignment, they create cash flow problems downstream that AR teams inherit with no context about why those terms exist or what was promised.

• Misaligned expectations at close. When sales oversells capabilities or delivery timelines to win a deal, the resulting client dissatisfaction often manifests first in payment behavior. The client is not technically disputing the invoice, they are expressing dissatisfaction through the one lever they still control. Finance sees a collections problem. The root cause is a sales execution problem.

• No handoff protocol. In most businesses, the transition from 'closed won' to 'client' is informal. Contact preferences, communication history, and relationship context stay in the salesperson's head or CRM notes. When the first invoice goes out, finance is reaching out to a client they have never spoken to, with no understanding of the relationship's texture. This is a structural setup for a poor first billing interaction.

What Revenue-Aligned AR Actually Looks Like

Fixing this does not require a full organizational restructure. It requires three deliberate changes:

• Shared data infrastructure. AR payment data should be visible to customer success and, for major accounts, to sales. Changes in payment behavior should trigger notifications to the relationship owner, not just to the collections queue. This is a systems decision, not a headcount decision.

• A defined handoff protocol. When a deal closes, the AR team should receive a structured brief: key contacts, communication preferences, any non-standard terms, and any delivery commitments that could affect payment timing. This takes minutes to create and prevents months of avoidable friction.

• Tone alignment between sales and collections. The way a client was sold to sets an expectation for how they will be communicated with throughout the relationship. A high-touch enterprise sale followed by a generic dunning email sequence is a jarring inconsistency. Collections outreach should be calibrated to match the relationship register that sales established, not default to a template built for accounts nobody cares about losing.

The Competitive Angle Nobody Talks About

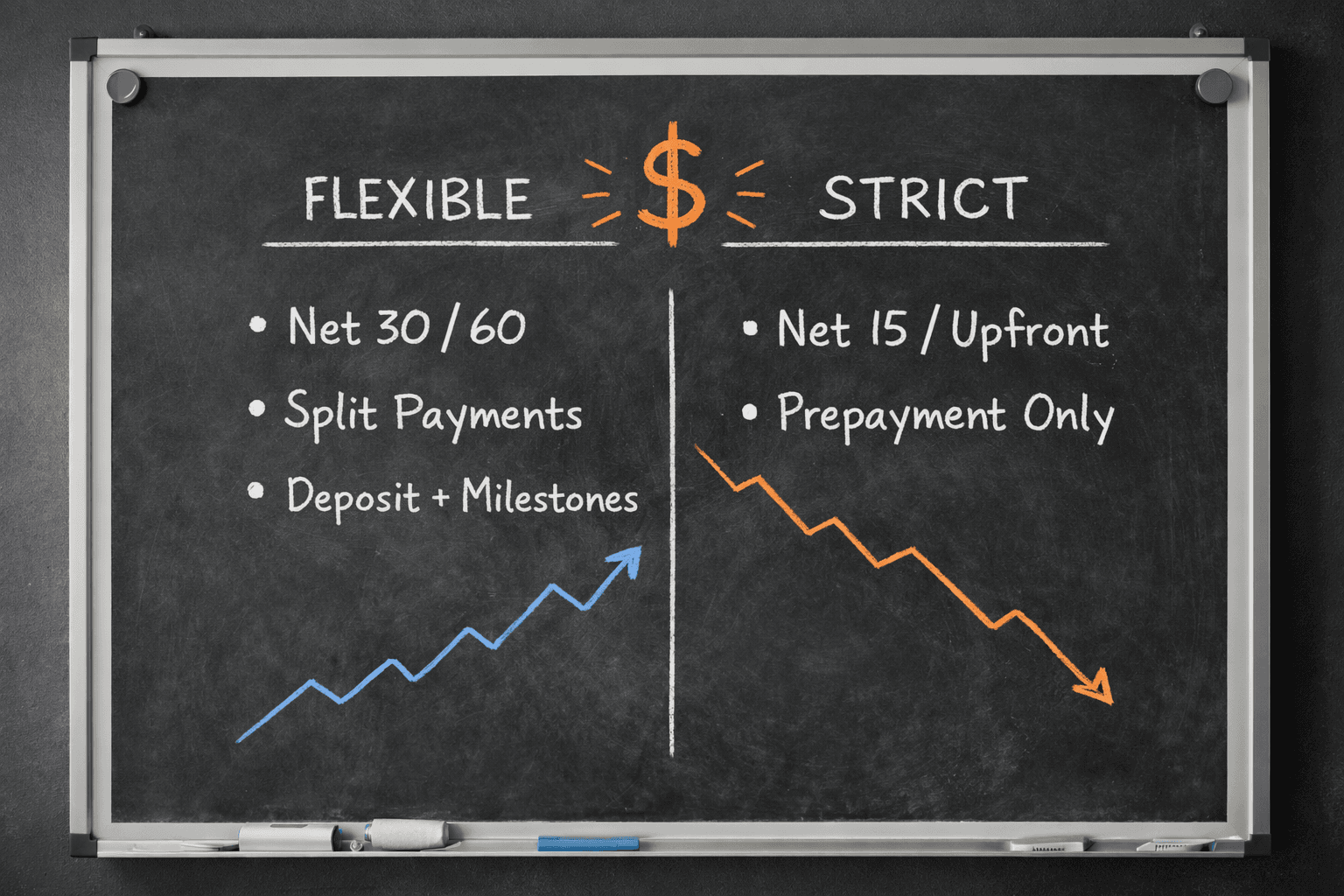

There is a commercial dimension to this argument that goes beyond retention. Businesses with clean, professionally managed AR processes can offer more flexible payment terms with confidence, because they have the infrastructure to enforce them consistently. That is a genuine sales advantage in competitive deals where payment flexibility is a differentiator.

Conversely, businesses with poor AR processes are often forced to tighten terms preemptively, demanding upfront payment or net 15 terms, not because the client is risky, but because their own collections process cannot handle anything more complex. They are penalizing good clients for their own operational weakness.

Revenue-aligned AR removes that constraint. When your collections process is sophisticated enough to manage flexible terms reliably, your sales team can compete on payment flexibility without finance losing sleep over cash flow predictability.

The Reframe

Accounts receivable is the final interaction your business has with a client in every billing cycle. It determines whether they feel respected or chased. Whether your process feels professional or amateur. Whether the relationship your sales team spent months building gets reinforced or quietly eroded.

That is not a finance problem. It is a revenue problem. And the businesses that treat it as one, connecting AR data to customer health monitoring, aligning collections tone to relationship context, and giving sales visibility into payment behavior, will find that their AR function is doing more than recovering cash. It is protecting the customer base that everything else depends on.

The last mile of the revenue cycle deserves the same strategic attention as the first.