Effective Credit Checks: Vetting Customers Before Extending Payment Terms

A credit check before extending payment terms is your cheapest bad-debt insurance. How to vet B2B customers fast, set the right terms, and avoid slow payers.

Pratheek Adi

Co-Founder & CTO

Table of contents

Share

A credit check is the fastest, cheapest way to avoid a slow payer. It is a short pre-terms review that tells you whether to extend Net 30, ask for a deposit, or sell on prepay only. It matters because 43% of US B2B credit sales were overdue in 2025 (Atradius, 2025), so a few minutes of vetting is insurance against an invoice you never collect.

The Hidden Cost of Trusting the Wrong Customer

A single uncollected invoice can do more than throw off your cash flow. It can trigger a chain reaction that touches payroll, vendor relationships, and your ability to invest in growth. Yet many businesses still extend payment terms based on gut feeling rather than hard data.

In the United States, about 43% of B2B invoiced sales were overdue in 2025, and bad debt continues to weigh on credit-based B2B sales. Both trends contribute to serious cash-flow pressure and higher write-offs. In Europe, an estimated 25% of bankruptcies are linked to late customer payments, which shows how quickly unpaid invoices can escalate into existential problems for a business. These figures come from aggregated research on B2B payment delays and accounts receivable performance by specialist AR and collections platforms.

The good news is that most payment defaults are predictable and preventable. With systematic credit checks and a structured evaluation process, you can reduce risk while still saying yes to the right customers. This article looks at why credit checks matter, how to run them effectively, and how frameworks like the 5 Cs of credit help you make smarter decisions before offering net terms.

For invoice-heavy, service-based businesses, this is not theory. It is a practical way to protect working capital and keep your collections team out of constant fire-fighting mode.

The Real Cost of Skipping Credit Checks

When you extend payment terms without proper evaluation, you are providing an unsecured loan. Any lender needs to know two things: can the borrower repay and will they repay.

Direct financial losses from bad debt are only part of the story. One analysis of large enterprises found that the average bad-debt-to-sales ratio was about 1.5%, with bad debt growing quickly over recent years. For a business generating 5 million dollars in annual revenue, that can mean more than 70,000 dollars in uncollectible invoices each year.

The hidden costs often hit harder:

A high share of overdue invoices forces finance leaders to spend more time forecasting cash and juggling payables.

Collections staff and account managers burn hours chasing payments instead of supporting customers or pursuing new opportunities.

Late payments strain relationships with your own suppliers and partners when you cannot pay them on time.

Many businesses owners report that late payments delay or derail long-term growth plans, such as expansion, hiring, or new service lines.

Credit checks are your first line of defense. They help you:

Identify customers who are likely to pay on time.

Spot red flags early and adjust terms before problems arise.

Set appropriate credit limits that balance revenue opportunity with risk.

A few minutes of structured credit evaluation before onboarding a new account is almost always cheaper than months of chasing overdue invoices later.

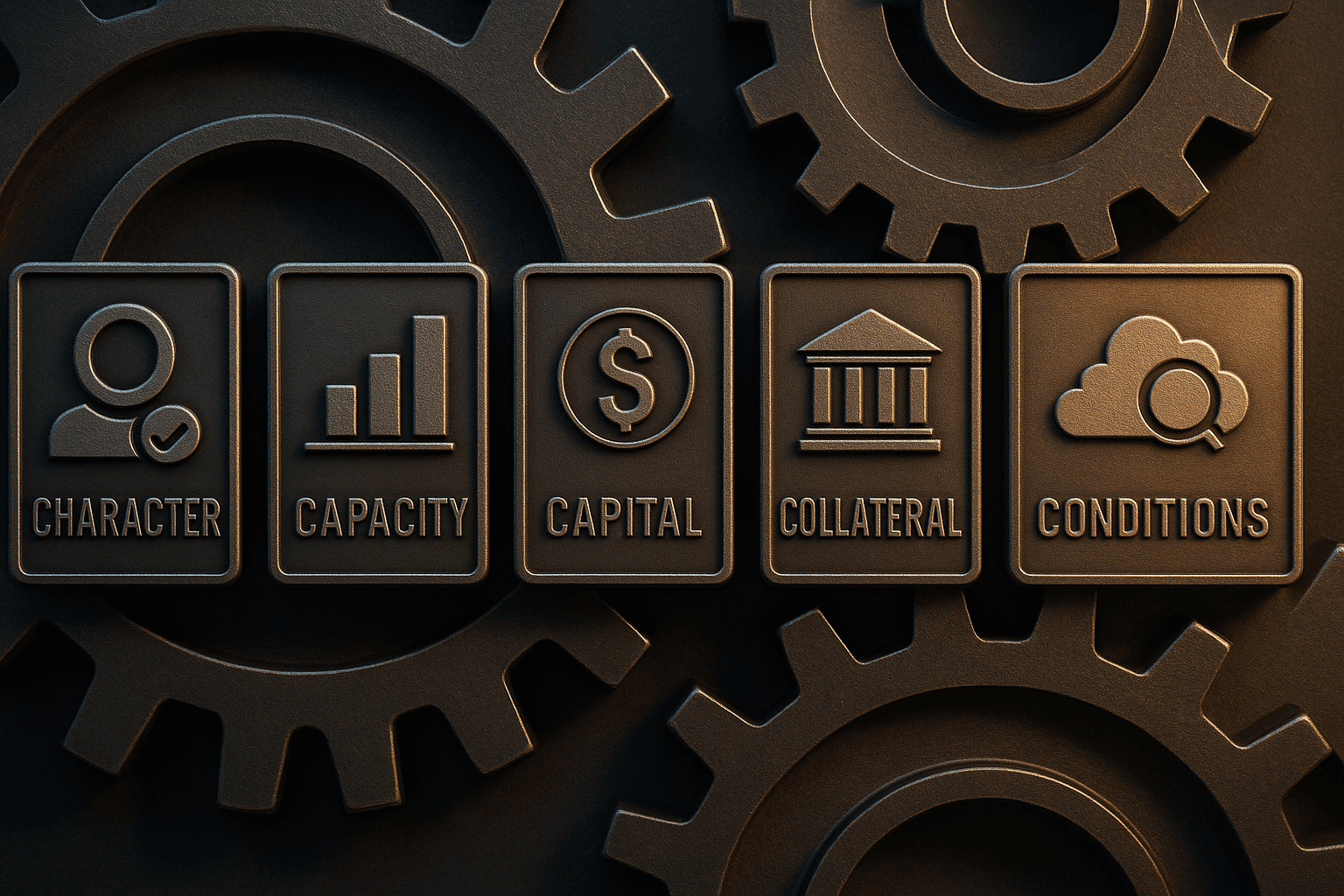

The 5 Cs of Credit: Your Framework for Evaluation

Financial institutions use the 5 Cs of credit to evaluate borrowers. The same framework works extremely well for service-based SMBs and startups that offer net terms.

1. Character

Character is about trust and behavior over time. It answers the question, “Does this customer have a history of paying what they owe?”

You can assess character by:

Reviewing business credit reports that show payment trends, past dues, and any collections or legal actions. Major bureaus like Dun & Bradstreet, Experian, and Equifax aggregate this information into scores and indices.

Looking at the length of time the business has been operating and any major ownership changes.

Requesting trade references from existing suppliers and asking specific questions like, “How long have they been a customer?” and “Do they usually pay within terms?”

A strong track record with other vendors is one of the best predictors of how they will treat you.

2. Capacity

Capacity measures the ability to pay, based on revenue and cash flow.

For larger credit exposures, you can:

Review income statements and cash-flow statements to see whether the business consistently generates enough cash to meet its obligations.

Use simple ratios, such as a debt-to-income ratio or interest-coverage ratio, to see how stretched they are.

Look for stable, recurring revenue rather than highly seasonal or one-off project revenue where cash inflows may be choppy.

Service-based customers with predictable monthly work and a diversified client base generally show stronger capacity than those dependent on a small number of big contracts.

3. Capital

Capital refers to the financial cushion the customer has built.

You can gauge capital by:

Reviewing balance sheets to see assets, liabilities, and owners’ equity.

Checking whether the business retains profits or operates with very thin equity and high leverage.

Looking at how much the owners have invested and whether they have a history of reinvesting.

Stronger capital means the business can absorb temporary setbacks without immediately defaulting on supplier payments.

4. Collateral

In many service businesses, you will not take formal security or liens on assets, but collateral is still a useful lens. It tells you what the customer could use to raise cash if they needed to.

Relevant questions include:

Does the business own significant equipment, inventory, vehicles, or property?

Does it have a strong receivables book of its own that could be financed?

You might not hold direct collateral, but understanding asset strength helps you decide how far to extend terms and whether to require partial payment up front.

5. Conditions

Conditions are the external factors that impact a customer’s ability to pay.

This covers:

Overall economic conditions in their region.

Industry trends, such as declining demand, new regulation, or rapid cost inflation.

Customer concentration risk, for example, a business that depends on one large contract for most of its revenue.

Two customers with similar financials can carry very different risk profiles if one operates in a stable, growing sector and the other in a highly volatile or declining one.

The strength of the 5 Cs framework is that strength in one area can offset weakness in another. For example, a newer business with limited credit history, but strong cash flow and high owner investment, might still qualify for reasonable limits, even if you keep terms shorter at first.

Essential Credit Check Methods and Tools

Once you understand what to look for, you need practical tools to gather the information.

Business credit reports

Business credit reports are usually your fastest starting point. They consolidate:

Payment history and trends with other suppliers.

Public records such as liens, judgments, and bankruptcies.

Risk scores that predict likelihood of delinquency or default.

Services from Dun & Bradstreet, Experian, Equifax, and aggregators like Creditsafe or Nav provide different scoring models. For example, Dun & Bradstreet’s PAYDEX score uses a 1 to 100 scale based on how promptly a business pays its bills.

Reports typically cost a fairly small amount per company and can save you from extending thousands of dollars of risky credit.

Financial statement and bank analysis

For larger or strategic customers, go beyond scores and look at financial documents.

Ask for recent balance sheets, income statements, and cash-flow statements.

Calculate simple ratios such as:

Current ratio (current assets divided by current liabilities) to test liquidity.

Debt-to-equity ratio to see how leveraged the business is.

Gross margin to understand operating efficiency.

Review several months of bank statements to confirm inflows, outflows, and cash buffers.

This level of analysis is especially useful when you are considering higher credit limits or long-term service contracts.

Trade references

Trade references give you real-world insight into how the customer behaves after the contract is signed.

Ask existing suppliers:

How long they have worked with the customer.

What terms they use.

Whether payments arrive on time or only after multiple reminders.

Whether there have been frequent disputes or write-offs.

Clear, specific feedback from trade references often tells you more about character than any score.

Credit applications

A structured credit application is your entry point to all of this information. It should capture:

Legal entity name and ownership structure.

Registered address and contact details.

Bank references and trade references.

Consent for you to obtain credit reports and verify information.

Have your legal counsel review your credit application template so that it properly authorizes you to collect and use this data in line with local regulations.

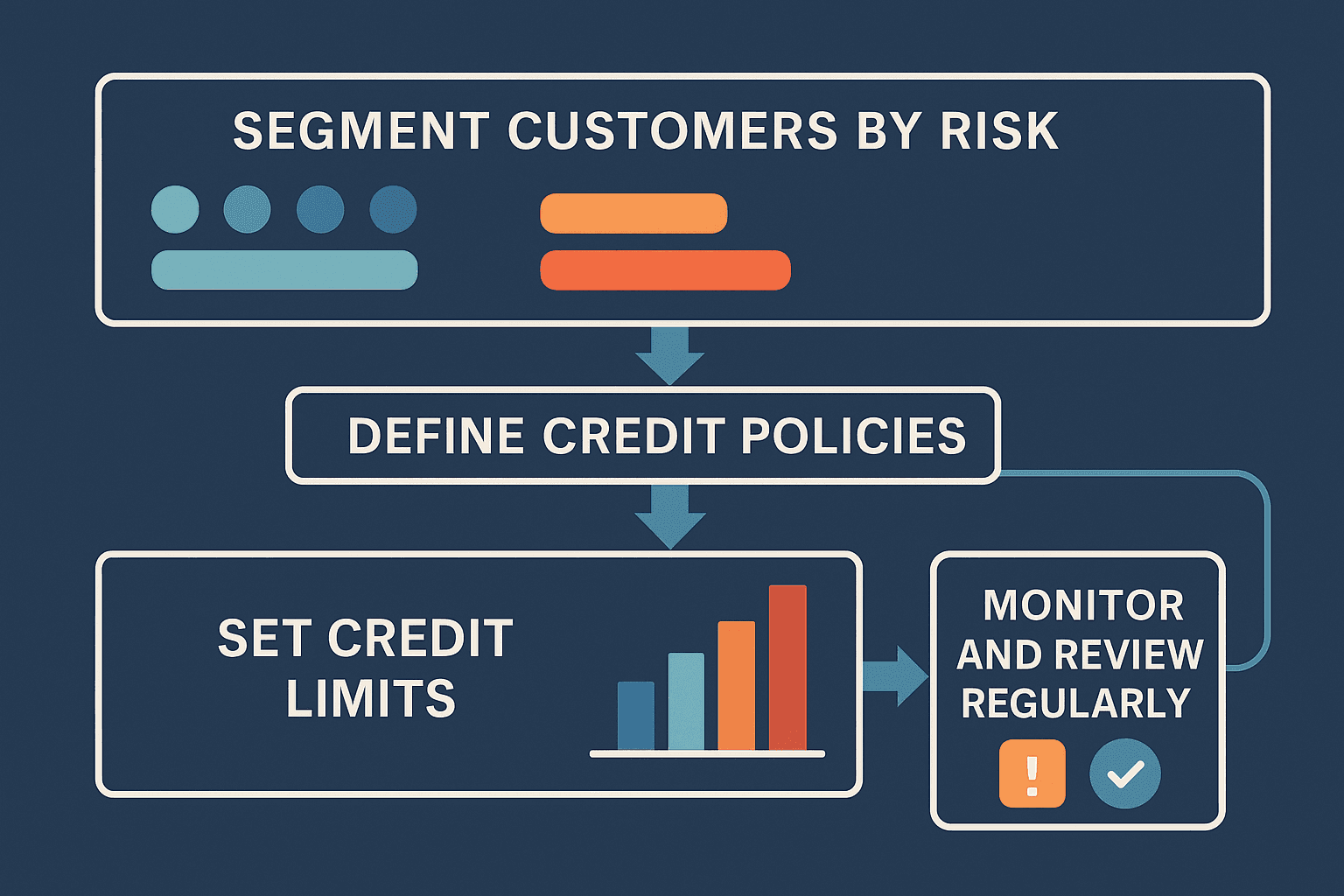

Building a Credit Evaluation Process That Scales

Most organizations run into problems not because they lack tools, but because they lack a repeatable process.

Segment customers by risk

Not every customer needs the same amount of scrutiny. You can:

Approve very small credit limits based on a clean, basic bureau report.

Require deeper analysis for customers whose projected monthly spend exceeds a certain threshold.

Treat key strategic accounts as a special segment with more frequent reviews.

This keeps your team from over-analyzing low-risk accounts while still protecting large exposures.

Define and document credit policies

Create a written credit policy that covers:

Minimum information required before granting terms.

Which scores or ratios are acceptable in different risk bands.

How to set initial credit limits and when to review them.

Approval workflows and who can override recommendations.

A clear policy makes decisions more consistent, reduces bias, and makes it easier to onboard new team members.

Set practical credit limits

When you set a limit, think in terms of real exposure rather than what the customer requests.

Consider:

Expected monthly or project volume.

Invoice frequency and typical payment cycles.

Customer financial health and industry risk level.

Start conservatively for new customers. You can always increase limits after a few months of clean payment history.

Monitor and review regularly

Credit evaluation is not “set it and forget it.” Schedule:

Annual or semi-annual reviews for most customers.

More frequent reviews for large or higher-risk accounts.

Automated alerts when credit scores drop or invoices drift beyond terms.

The goal is to spot deteriorating conditions early so you can tighten terms, reduce limits, or require deposits before balances grow too large.

Red Flags That Signal Higher Credit Risk

Experienced credit managers develop instincts about risk, but you can codify many warning signs.

Common red flags include:

Incomplete or inconsistent applications with missing sections, conflicting addresses, or frequent changes in company details.

Reluctance to provide financial information for a credit request that would materially expose your business.

Poor payment history in bureau reports or from trade references, including frequent late payments or prior defaults.

Unusually high leverage or low liquidity in financial statements, for example a very high debt-to-equity ratio or a current ratio well below 1.

Aggressive behavior, such as pressuring you to rush approval or pushing for very high limits that are out of line with their size and track record.

A red flag is not always an automatic “no,” but it is a clear signal to dig deeper. You might respond by lowering the initial limit, shortening payment terms, asking for a deposit, or requiring a director guarantee before proceeding.

Practical Takeaways: Your Credit Check Action Plan

If you want to strengthen your credit process right away, you can:

Require a formal credit application for every new customer that wants payment terms.

Pull at least one business credit report before granting credit above your risk threshold.

Use a tiered approval workflow, with automated approvals for small, low-risk requests and manual review for higher exposures.

Set credit limits based on financial capacity, not just requested amounts, and revisit them once the customer builds a track record.

Put your credit policy in writing and train your finance, sales, and operations teams on how it works.

Request trade references and actually call or email them with specific questions about payment behavior.

Calculate a few simple ratios for larger accounts so that risk decisions are grounded in numbers, not intuition alone.

Schedule regular reviews of existing customers, especially in volatile sectors.

Watch payment behavior from the first invoice and address slippage quickly, even if the customer seems important.

Consider credit insurance for very large or international exposures where a single default would materially hurt your business.

How Automation Strengthens Your Credit Process

Credit evaluation involves a lot of moving parts: applications, reports, approvals, and ongoing monitoring. If you are processing 500 or more invoices per month, manual work will eventually become a bottleneck.

Modern accounts receivable tools help you:

Pull credit reports automatically from one or more bureaus when a new application arrives.

Auto-score customers according to your 5 Cs criteria and credit policy.

Route low-risk cases for instant approval and escalate higher-risk ones to a credit manager.

Monitor changes in credit scores and payment behaviour over time and trigger reviews when thresholds are crossed.

Abivo takes this a step further for service-based SMBs and startups by combining credit discipline with automated collections. Once you have set terms and limits, Abivo’s AI agents handle the repetitive work of invoice follow up by phone and email. The platform connects directly to tools like QuickBooks, NetSuite, FreshBooks, Sage Invoicing, Microsoft Dynamics, Xero, Stripe, Square Invoices, SAP Business One and Ariba, Jobber, ServiceTitan, BuildOps, and Bill.com, so your credit decisions flow seamlessly into your invoicing and collections process.

The result is a closed loop: better vetting on the front end and smarter, automated follow up on the back end, all with less manual effort from your finance team.

For more on setting terms, see our guide to DSO benchmarks by industry and why late payment is really a follow-up problem.

Turning Credit Checks Into Competitive Advantage

Effective credit checks do more than prevent losses. They help you grow with confidence.

When you have a clear, data-driven process, you can:

Approve good customers faster than competitors who rely on slow, manual reviews.

Offer appropriate limits and terms that support your customers’ growth without putting your own cash flow at risk.

Say no, or “not yet,” to risky customers before you invest time and resources that you may never recover.

Think of credit evaluation as part of your broader risk and customer strategy, not a roadblock to sales. Even a simple, consistent process puts you ahead of many peers that extend terms purely on trust. Over time, your receivables will become more predictable, your team will spend less time chasing overdue invoices, and you will have more working capital available for growth.

Start with the basics: apply the 5 Cs, put your policy in writing, and use automation where it makes sense. As you refine your approach, you will find that strong credit checks are not just a safeguard, they are a competitive advantage for any service-based business that lives on invoicing.

Want vetting and follow-up handled automatically? Get Started with Abivo.

Frequently Asked Questions

What is a B2B credit check?

A pre-terms review of a business customer’s ability and history of paying: credit reports, trade references, payment history, and public records like liens and judgments. It tells you what terms to safely extend.

How long should a credit check take?

For most accounts, minutes. A quick report plus one or two trade references is enough to decide between standard terms, a deposit, or prepay. Save deep dives for large credit lines.

What credit limit should I extend a new customer?

Start conservative and let the account earn more. Tie the initial limit to the customer’s size, the order size, and the credit signals, then raise it as they build a clean payment history with you.

Do credit checks actually reduce bad debt?

They reduce the odds of extending terms to a customer who cannot or will not pay. With 43% of US B2B sales overdue in 2025, vetting before you ship is far cheaper than chasing after.

How often should I re-check existing customers?

Re-check at renewal, before a credit-limit increase, or the moment an account starts paying late. A customer who was solid two years ago can be stretched today.