How Late Payments Hurt Your Business Valuation (and What to Do About It)

Discover how chronic late payments and high DSO directly shrink your business valuation through working capital adjustments, DCF penalties, and multiple compression, and learn proven strategies to protect your worth.

Soham Gawde

Business Analyst

Table of contents

Share

When Unpaid Invoices Quietly Steal Your Company’s Worth

Every business owner knows late payments strain cash flow. But few realize that chronic delays and rising Days Sales Outstanding (DSO) actively shrink your company’s valuation, not just operationally, but on paper. Whether you plan to sell, raise capital, or simply build a more valuable asset, outstanding receivables act as a silent thief. They rob your balance sheet of liquidity, compress valuation multiples, and signal risk that investors and lenders price into every dollar of your company’s worth.

The connection between collections and valuation is direct and measurable. A business with $2 million in annual revenue and a DSO of 65 days carries significantly less value than an identical competitor collecting in 30 days. The difference shows up in discounted cash flow models, working capital adjustments during due diligence, and the multiple buyers are willing to pay. Understanding this relationship is the first step toward protecting and maximizing what you have built.

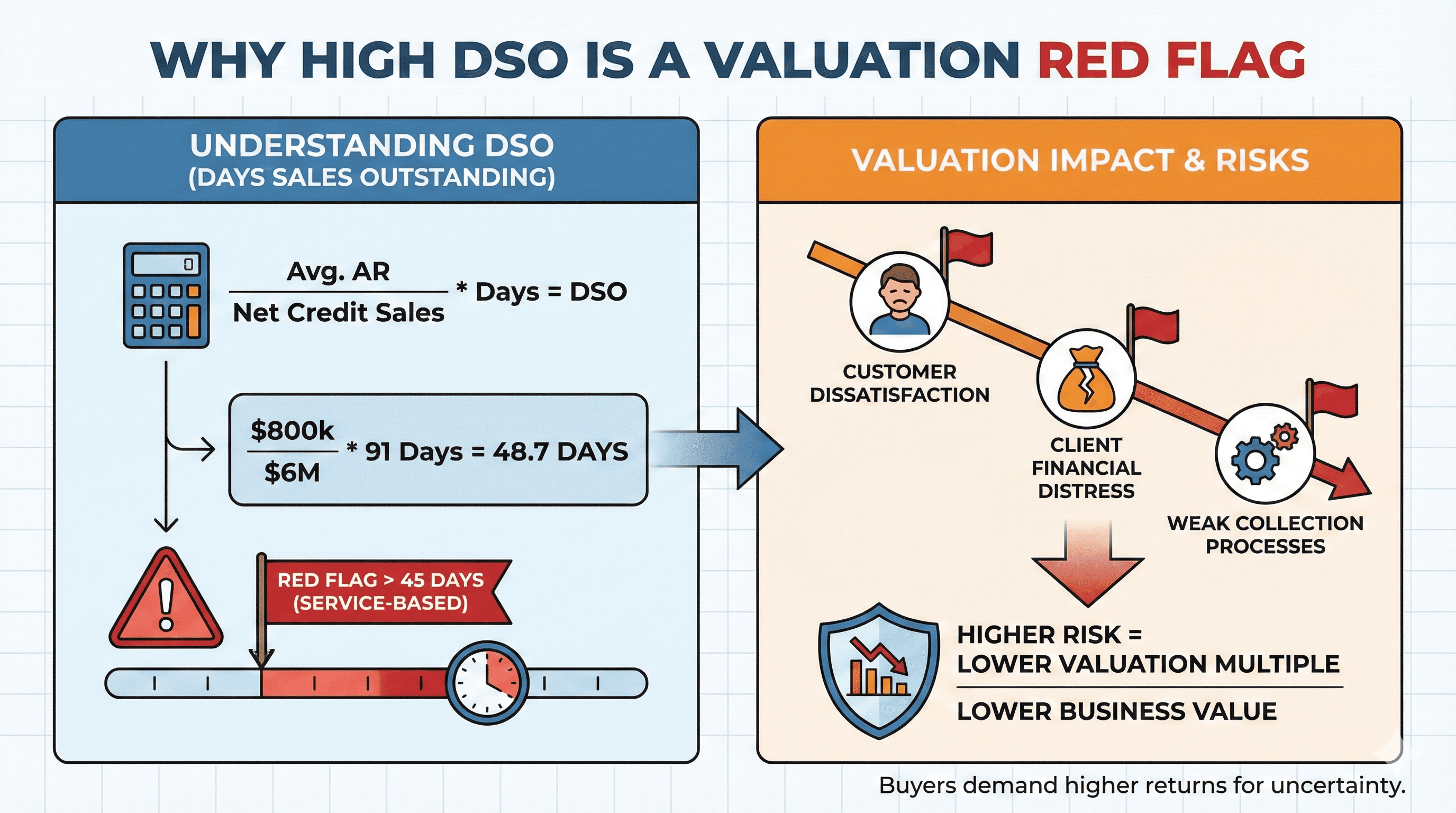

Why DSO Is a Valuation Red Flag

Days Sales Outstanding measures how long it takes to collect payment after a sale. The formula is straightforward: divide average accounts receivable by net credit sales, then multiply by the number of days in the period. For a company with $800,000 in receivables and $6 million in quarterly credit sales, DSO equals 48.7 days. While benchmarks vary by industry, anything substantially above 45 days for service-based businesses signals collection inefficiency.

Investors and valuation analysts treat DSO as a primary indicator of operational health. A climbing DSO suggests customers are paying slower, which may indicate customer dissatisfaction, financial distress among clients, or weak internal collection processes. Each of these interpretations raises the risk profile of your business. Higher risk translates directly into a lower valuation multiple, because buyers demand higher returns to compensate for uncertainty.

The Three Mechanisms That Shrink Your Value

1. Working Capital Adjustments Slash Purchase Price

In mergers and acquisitions, buyers negotiate a net working capital (NWC) target. Working capital equals current operating assets minus current liabilities, with accounts receivable being the largest component for most service businesses. If your actual working capital at closing falls below the target, the purchase price drops dollar for dollar.

Consider a professional services firm with $1.5 million in receivables and sluggish collections. If working capital is $200,000 short of the target, the buyer reduces their offer by $200,000 to inject the missing liquidity. This adjustment happens automatically in most deals. Worse, if the shortfall stems from old, uncollectible receivables, you absorb the loss while the buyer gains a business with clean books.

Excess working capital has the opposite effect, but many owners misunderstand what “excess” means. Keeping cash tied up in receivables is not excess, it is inefficiency. Buyers will not pay a premium for your poor collection practices. They will either discount the price or demand you clean up the balance sheet before closing.

2. DCF Models Penalize High DSO Through Reduced Free Cash Flow

The Discounted Cash Flow (DCF) method values a business by projecting future cash flows and discounting them to present value. Free Cash Flow (FCF) is calculated as operating cash flow minus capital expenditures and changes in working capital. Here is where DSO inflicts damage: every day of sales locked in receivables increases working capital, which reduces FCF.

If your DSO rises from 35 to 55 days, you tie up additional cash in receivables. That increase is subtracted from FCF, lowering the present value of your business. Two identical companies generating AED 1 million in profit will have vastly different valuations if one frees up cash through efficient collections while the other traps it in aging invoices. Over a five-year projection period, even modest DSO improvements can add hundreds of thousands of dollars to valuation.

3. Valuation Multiples Compress Due to Perceived Risk

Valuation multiples, such as EV/EBITDA or revenue multiples, reflect market perceptions of risk and growth. Buyers apply higher multiples to predictable, low-risk cash flows and lower multiples to volatile, high-risk earnings. Chronic late payments trigger multiple compression through several channels.

First, they erode creditworthiness. Frequent late payments reported to business credit bureaus drastically reduce your company’s credit score. A lower score signals financial instability, pushing buyers to apply a higher discount rate (and thus a lower multiple) to your future earnings.

Second, they constrain growth. Capital tied up in receivables cannot fund marketing, hiring, or equipment upgrades. A business that cannot reinvest stagnates, making it a less attractive acquisition target. Mid-sized companies in technology, healthcare, and professional services are hit hardest: 40.9% face severe cash flow disruption, and 8.3% lose over 10% of annual revenue due to late payments.

Third, they create operational drag. Employees spend time chasing invoices instead of serving customers. Suppliers tighten credit terms. Stress and burnout increase among leadership. These inefficiencies show up in due diligence as red flags that justify a lower offer.

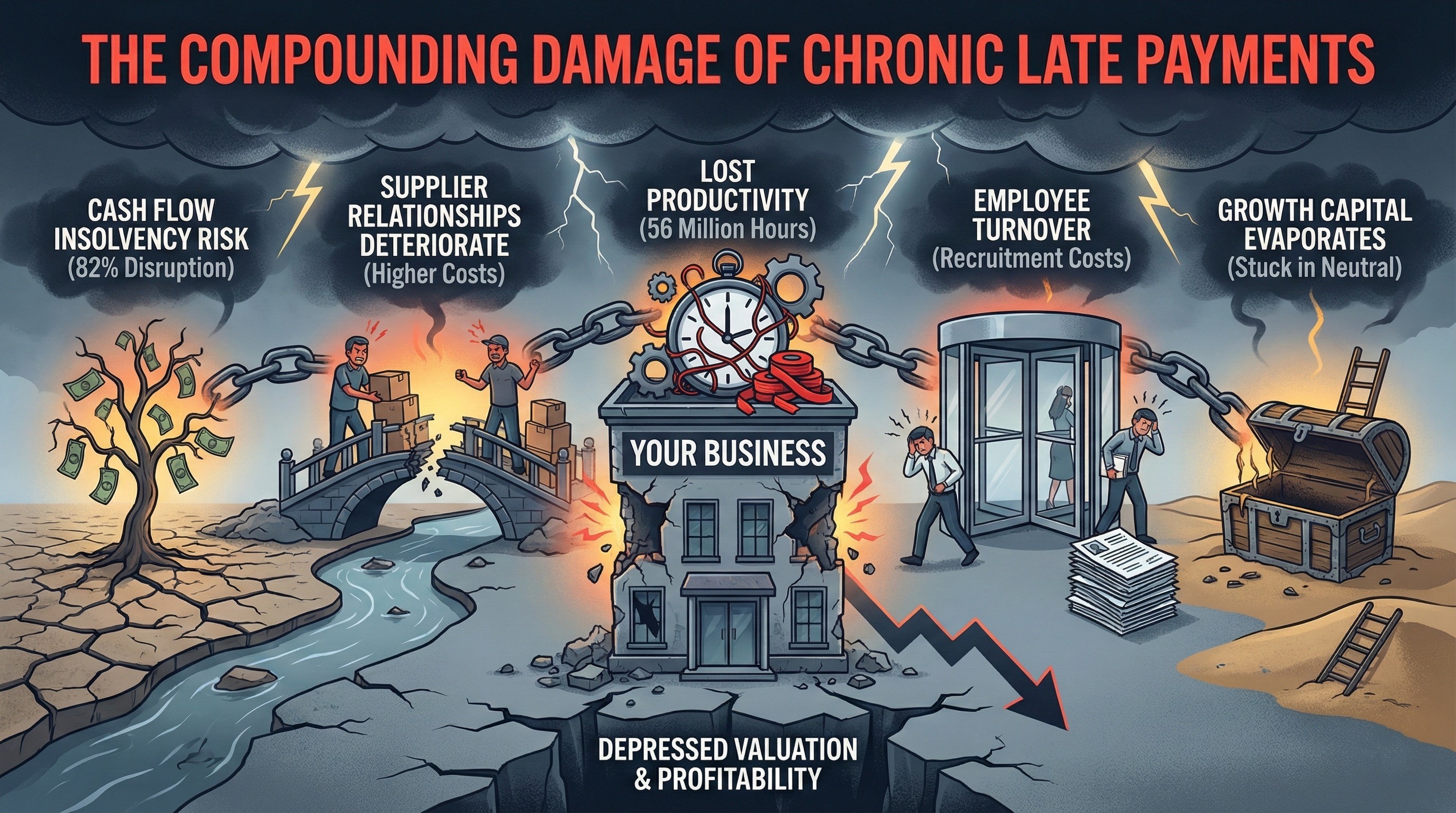

The Compounding Damage of Chronic Late Payments

The impact extends beyond valuation mechanics into every corner of your business:

Cash Flow Insolvency Risk: 82% of businesses report moderate to critical cash flow disruption from late payments. When you cannot cover payroll or supplier obligations, you may take on expensive debt or delay critical payments, further damaging your credit profile.

Supplier Relationships Deteriorate: Late payments to vendors become inevitable when customers do not pay you. Suppliers respond by raising prices, cutting credit lines, or terminating relationships. This increases your cost structure permanently, reducing EBITDA and valuation.

Lost Productivity: UK small businesses lose 56 million hours annually chasing late payments. That is time not spent on revenue-generating activities. The administrative burden alone can cost more than the original invoice value.

Employee Turnover: Payroll stress leads to dissatisfaction and exits. High turnover increases recruitment costs and disrupts client service, creating a negative feedback loop that depresses profitability.

Growth Capital Evaporates: Businesses need cash to seize opportunities. When funds are trapped in receivables, you cannot invest in new equipment or enter new markets. Even profitable companies can become stuck in neutral.

Real-World Impact: What the Data Shows

The scale of the problem is staggering. Small and medium enterprises report that 11% of all invoices are paid late, representing nearly $1 trillion annually in delayed payments. In the UK, 26% of businesses say late payments have become more common in the past year, with the average value rising to £62,000.

The consequences are severe. The Federation of Small Businesses estimates that 50,000 business closures could be avoided each year if invoices were paid on time. In the US, businesses are owed an average of $304,066 by late-paying clients. Technology and SaaS firms suffer disproportionately: 44.4% report severe cash flow disruption, and 22.2% lose over 10% of annual revenue due to collection issues.

For businesses on net payment terms producing over 500 invoices monthly, these numbers are not abstract—they represent a direct assault on enterprise value.

Breaking the Cycle: Proven Strategies to Protect Valuation

Tighten Credit Policies and Payment Terms

Review customer credit limits annually. Require deposits for large projects. Offer early payment discounts (e.g., 2/10 net 30) to incentivize speed. Clear terms in contracts reduce disputes and set expectations.

Automate Invoicing and Collections

Manual processes create delays. Automated systems send invoices immediately, schedule reminders, and escalate past-due accounts systematically. This reduces DSO by 30-40% in most implementations.

Implement Dynamic Collections Workflows

Segment customers by risk and payment history. High-risk accounts receive more frequent touchpoints. Low-risk customers get gentle nudges. This focuses effort where it matters and preserves relationships with reliable clients.

Use Data to Predict and Prevent

Track DSO by customer, invoice type, and time period. Identify patterns, does DSO spike in Q4? Do certain industries pay slower? Use these insights to adjust credit terms proactively.

Consider Receivables Discounting Strategically

Selling invoices to a factor at a 1-5% discount provides immediate cash and transfers collection risk. This is not ideal for every invoice, but it can bridge gaps during growth phases or when cleaning up aged receivables before a sale.

Conduct Monthly Cash Flow Forecasting

Project collections based on historical DSO, not invoice due dates. This creates realistic budgets and highlights cash gaps before they become crises.

Action Steps for Business Owners

Calculate your current DSO monthly and track trends over time. A rising trend signals emerging problems.

Review your accounts receivable aging report weekly. Focus on invoices over 30 days past due.

Set clear payment terms in every contract and enforce late fees after two violations within 12 months.

Automate invoice delivery and payment reminders to eliminate manual delays.

Segment customers by payment behavior and tailor collection intensity accordingly.

Build a cash reserve equal to at least two months of operating expenses to buffer against late payments.

Normalize your financial statements before seeking valuation or sale, adjusting for personal expenses and non-recurring items.

Negotiate working capital targets early in any M&A discussion to avoid surprise price reductions.

How Automation Preserves Your Valuation

Tools like Abivo.ai help businesses recover revenue faster with less manual effort. By deploying AI calling and email agents that integrate with QuickBooks, NetSuite, Xero, and other platforms, Abivo reduces DSO through consistent, timely follow-up. The system identifies at-risk accounts, escalates appropriately, and frees your team to focus on growth rather than collections.

The result is a healthier balance sheet, stronger cash flow, and a business that commands a premium valuation. In a world where 50% of small business invoices are paid late, automation is not a convenience, it is a value protection strategy.

Turn Collections Into a Value Driver

Late payments and high DSO are not minor operational nuisances. They are direct threats to your company’s valuation, compressing multiples, reducing cash flow, and signaling risk to buyers and lenders. The damage compounds over time, eroding creditworthiness, stunting growth, and draining morale.

The good news is that improvement is achievable. By measuring DSO rigorously, tightening processes, and leveraging automation, you can transform collections from a cost center into a value driver. A business that collects quickly is more liquid, less risky, and ultimately worth more. Protecting your valuation starts with protecting your cash flow.