The Essential Year-End AR Cleanup Checklist

The year-end close doesn’t have to be a financial scramble. This guide breaks down a clear, three-phase approach: Reconciliation, Collection, and Compliance, to help finance teams clean up AR, strengthen cash flow, and lock in accurate, compliant financials before the new year begins.

Sia Ghazvinian

Co-Founder & CEO

Table of contents

Share

The Hidden Cost of the Year-End Scramble

For finance professionals and business owners, the end of the year often feels less like a strategic wind-down and more like a frantic dash to close the books accurately. This intense pressure frequently leads teams to rush through crucial accounting and collections tasks, leaving small and midsize businesses (SMBs) with inflated, inaccurate accounts receivable (AR) figures. When AR balances are overstated, it results in financial statements that mislead management and potential investors about the company's true liquidity and operational health.

The consequences of an uncleaned AR ledger are severe, impacting both immediate operations and long-term regulatory compliance. Failure to collect outstanding invoices or improperly address their status before the fiscal year closes can immediately trigger a cash flow crunch. This strain can hit particularly hard if the business faces seasonal lows or needs to cover large year-end expenses.

More critically, an improperly managed end-of-year AR process prevents businesses from maximizing potential tax deductions. If accounts are assessed and determined to be uncollectible, the business must ensure that all mandatory collection attempts are documented to prove the debt is legally worthless. Without this required evidence, the right to claim a business bad debt deduction is compromised, which can unnecessarily increase the business's tax liability for the year. Therefore, effective management of the year-end AR process must be systematic, moving beyond simple collections to encompass formal accounting reconciliation and regulatory compliance. This expert guide provides a systematic, three-phase checklist: Reconciliation, Collection, and Compliance, designed to effectively manage year-end AR cleanup and transform this traditionally painful process into a foundational strategic benefit.

Phase 1: Cleaning the Books with Expert Reconciliation

The foundation of a successful year-end close is ensuring that the accounts precisely reflect reality. This detailed cleanup must occur before any serious cash recovery efforts begin, guaranteeing that the business is making decisions based on accurate data.

Achieving Financial Clarity Through Detailed AR Reconciliation

Reviewing and Diagnosing the Aged Accounts Receivable Report

The Aged AR Report serves as the primary diagnostic tool for assessing the health of a company’s credit extension process. This report categorizes outstanding invoices into specific delinquency brackets, commonly including 0–30 days, 31–60 days, and 90+ days past the due date. Reviewing this report allows finance teams to quickly identify high-risk accounts that are long-overdue and require immediate action. Based on company policy, this diagnosis leads to crucial decision-making: escalating collections, offering a settlement, or formally assessing the account for write-off.

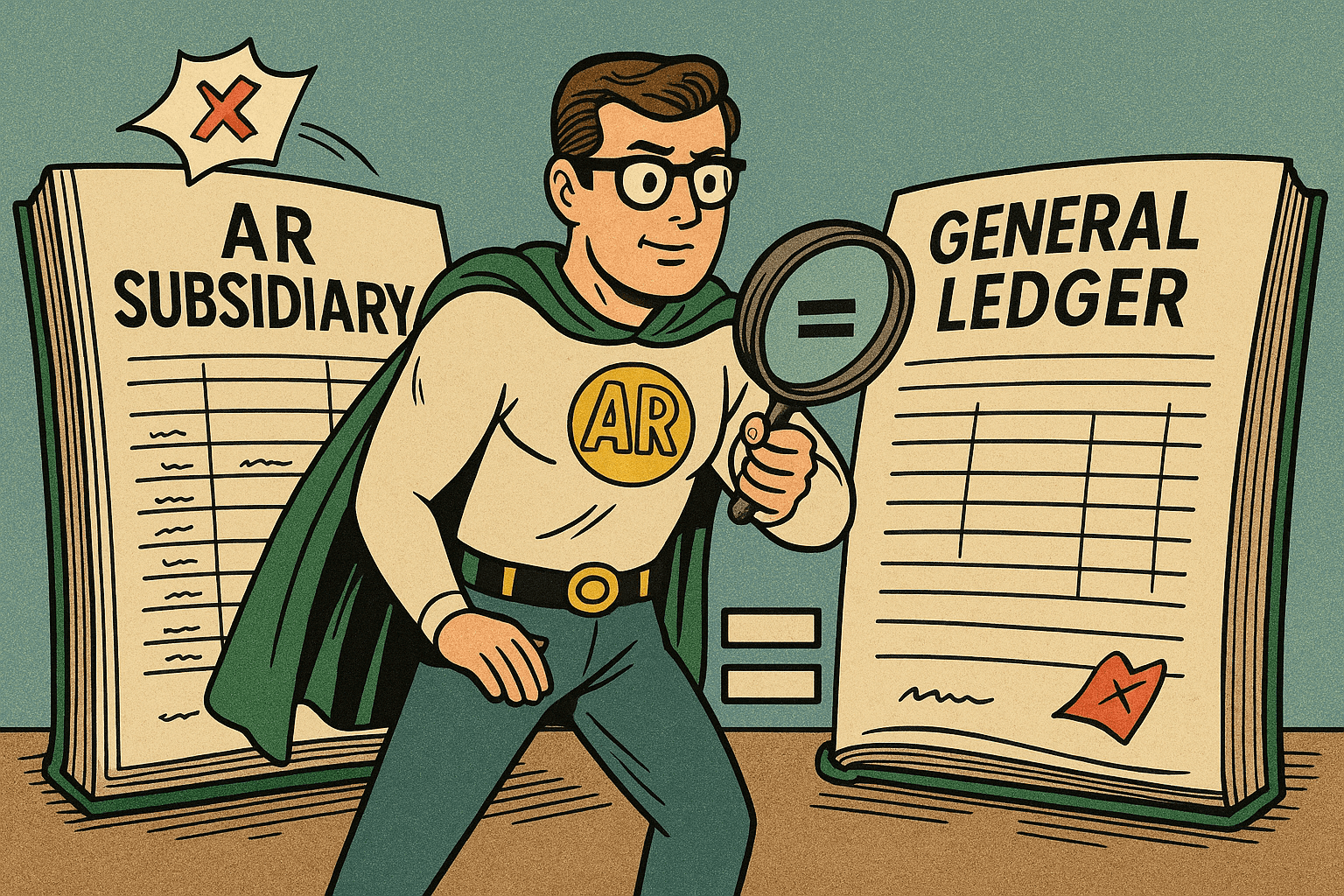

Reconciling the AR Ledger to the General Ledger

One of the most critical technical steps in the year-end close is performing a thorough AR reconciliation. This process ensures that the total balance derived from the collection of all individual customer AR accounts, which constitutes the subsidiary ledger, precisely matches the total balance recorded in the single Accounts Receivable control account in the General Ledger (GL). Discrepancies between the two are common and often arise from manual adjustments made directly to the GL without corresponding updates to the detailed subsidiary AR system, or they may stem from simple posting errors. Failure to resolve these variances before the year-end date leads to misstated balance sheet figures, which can cause significant issues during financial review or external audit.

Mastering the Cutoff Procedure for Accurate Revenue Recognition

The invoice cutoff procedure is a crucial internal control designed to ensure that revenue is recognized in the proper accounting period. For year-end purposes, this means revenue recognition must align with the date the service was rendered or the invoice was generated, not the date the payment was received or the entry was manually posted. Accountants must carefully scrutinize all transactions recorded immediately around the year-end date for instance, reviewing transactions from the last few days of December through the first few days of January to ensure they are placed in the correct fiscal year. This attention to detail is essential for accurate annual revenue reporting.

Clearing Out Unapplied Credits and Payments

Unapplied credits are balances sitting on a customer's account that have not been matched to a specific invoice; these often result from customer overpayments, unapplied deposits, or data classification errors. These credits obscure the true AR balance and must be resolved for a complete AR reconciliation. The process requires finance teams to identify and review all such credits.

Whenever possible, you should match the credits to corresponding open invoices to clear the discrepancy. If the credit is a true overpayment or prepayment, you must contact the customer to see if they prefer the credit applied to a future invoice or if they require a refund. This persistent issue of unapplied credits highlights a systemic failure in manual cash application processes. Tools that automate AR cleanup can drastically cut down on manual errors by using AI to match payments to invoices instantly, thereby preventing future year-end clutter.

Essential Year-End AR Reconciliation Tasks

Cleanup Task | Goal | Source Data | Key Action |

Review AR Aging Report | Identify overdue accounts and assess collectability risk. | AR Subsidiary Ledger | Categorize debts (0-30, 31-60, 90+ days) and flag high-risk accounts. |

Reconcile AR to GL | Ensure subsidiary records match the master accounts. | AR Aging Report and General Ledger | Investigate and resolve posting or manual adjustment errors. |

Manage Cutoff Dates | Record revenue and expenses in the proper accounting period. | Invoice Dates vs. Posting Dates | Review transactions around year-end to ensure revenue recognition is accurate. |

Resolve Unapplied Credits | Clear customer overpayments and credit balances. | Customer Ledgers/Account Statements | Match credits to open invoices or contact customers regarding refund/future application. |

Phase 2: Maximizing Cash Flow with Final Collection Efforts

With accurate figures confirmed in Phase 1, the next step is a strategic final collection push aimed at maximizing year-end cash balances. This effort must be focused, professional, and prioritized to yield the best results.

Implementing a Strategic Final Push for Outstanding Revenue

Prioritizing Strategic Collections Before the Clock Runs Out

Collections efforts at year-end must shift from simple volume to strategic targeting. It is necessary for finance teams to move beyond merely looking at aging buckets and conduct risk-based assessments. This approach prioritizes accounts based on their likelihood of payment, ensuring that resources are concentrated on high-probability recoveries while conserving time by not chasing accounts deemed truly worthless. The time frame spanning from 60 to 90 days past the due date is especially critical, representing the final internal recovery opportunity before escalation, such as external collections or formal write-off—becomes necessary.

Leveraging Professional, Urgent Communication for Recovery

In the business-to-business (B2B) environment, communication regarding late payments must be professional, firm, and focused on resolution. Effective follow-up often involves using phone calls or written notices that gradually increase in urgency. Rather than using an accusatory tone, which can damage future relationships, focus on proactive, positive language. For instance, when engaging a customer, ask, "When will you be able to pay?" instead of, "Why haven't you paid?". This approach frames the discussion around finding a solution and preserving the long-term relationship.

For the oldest, most difficult debts, preparation for escalation is key. This may involve preparing final demand letters or considering a settlement offer. Offering a reduced payment settlement can be significantly more advantageous than pursuing lengthy and costly legal action or sending the account to an expensive third-party collection agency.

How Automated Agents Protect Relationships and Prioritize Human Focus

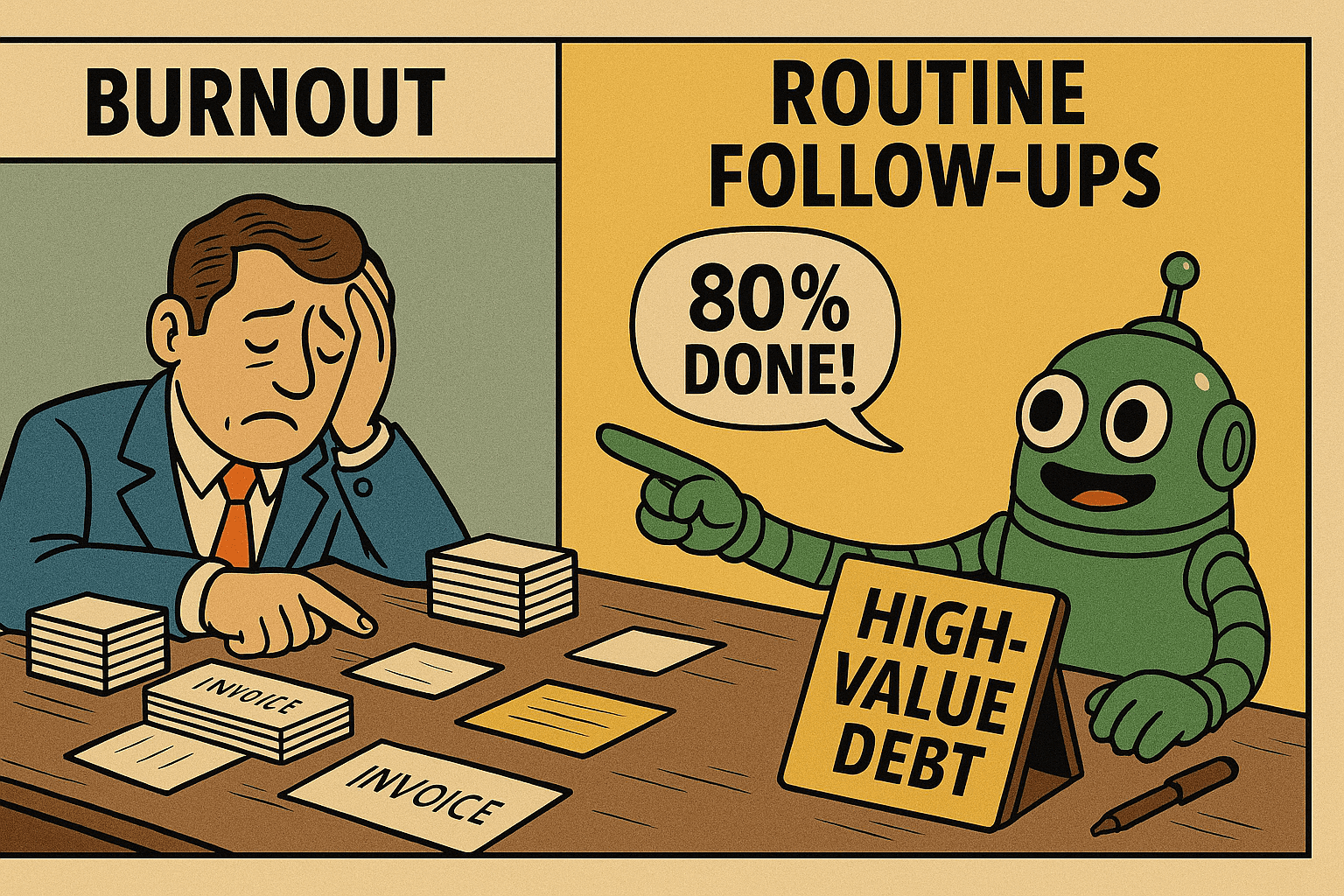

A common inefficiency in manual collections is that human staff spend the majority of their time on routine, low-risk reminders and administrative follow-ups, which diminishes focus and can lead to burnout. Automated collection tools, such as AI calling and email agents, can efficiently manage up to 80% of these routine communications, including early and mid-stage follow-ups.

This automation ensures that basic reminders are sent consistently and on time, which can significantly increase answer rates and immediate payments. This operational efficiency frees up human collections staff to focus exclusively on the complex, high-stakes negotiations required during the year-end push: settling large delinquent accounts, resolving intricate disputes, and maintaining key customer relationships. The final collections push, therefore, becomes less about high-volume manual work and more about focused human intervention on prioritized, high-value accounts.

Phase 3: Preparing for Tax Season and Bad Debt Compliance

Successfully managing tax season receivables requires a shift in focus from cash recovery to formal accounting compliance. The primary goal of this phase is ensuring that any debts deemed uncollectible meet the rigorous documentation standards required by the IRS for a business bad debt deduction.

Securing Tax Deductions: The Compliance and Write-Off Process

Establishing Worthlessness: The Non-Negotiable IRS Standard

Before any business debt can be deducted as an expense, the IRS mandates a strict standard: the debt must be 100% worthless. This means the business must realistically conclude that there is zero chance that the customer can or will ever pay the amount owed. To validate this conclusion to the IRS, the business must possess documented proof showing specific, professional efforts were made to recover the funds. This required documentation includes comprehensive records of letters, invoices, and phone calls. The availability of this detailed, time-stamped proof is what validates the decision to formally write off the asset.

Accounting Treatment: Accrual versus Cash Basis

The deductibility of bad debt is fundamentally tied to how the business recognizes revenue. A business can only claim a business bad debt deduction if the amount owed was previously included in the company's gross income from sales or services.

Businesses filing on the accrual basis follow the matching principle, meaning expenses are recorded in the same period as the related revenue. They typically estimate future losses using the Allowance for Doubtful Accounts (AFDA), which is a contra-asset account, paired with a corresponding Bad Debt Expense (BDE). This methodology ensures that financial statements provide an accurate portrayal of net income and reflects a more realistic net realizable value of AR on the balance sheet.

Businesses using the simpler cash basis generally recognize income only when cash is received. When a debt proves worthless, the typical accounting method is to issue a credit memo linked to the original income account, effectively netting the revenue for that specific invoice to zero. Given the potential complexity of credit memo accounting and its specific impacts on a business’s Profit and Loss statement, consultation with a certified public accountant (CPA) is strongly recommended to confirm the correct method for the specific entity.

Reporting Business Bad Debt for Tax Filing

The form used to deduct business bad debt depends entirely on the company’s legal structure. For example, sole proprietors typically deduct bad debt on Line 27a of Schedule C (Form 1040). S Corporations report the deduction on Form 1120-S. It is important to note that any worthless debt that does not meet the criteria of "business debt" (such as a personal loan) is treated differently, usually as a short-term capital loss, and must be reported on Form 8949. Ensuring that debts are categorized and reported correctly is a crucial component of year-end compliance.

Documenting Worthless Debt for Tax Compliance

Requirement for Bad Debt Deduction | Compliance Standard | Necessary Documentation (Proof) |

Must be Business Debt | Amount owed must have been previously included in gross income from sales or services. | Original contracts, detailed invoices, revenue recognition records. |

Must be 100% Worthless | There must be no reasonable chance of collection. | Formal internal write-off memo, evidence of legal review (if applicable). |

Documented Effort to Collect | Evidence of continuous, professional attempts to recover funds is mandatory. | Standardized collection letters/emails, phone call logs, automated audit trails.17 |

Proper Tax Filing | Report the business debt correctly based on the entity type (e.g., Schedule C, Form 1120-S). | Consult with a CPA to ensure correct form usage and deduction timing. |

Automation as Your Year-End Co-Pilot: Compliance and Efficiency

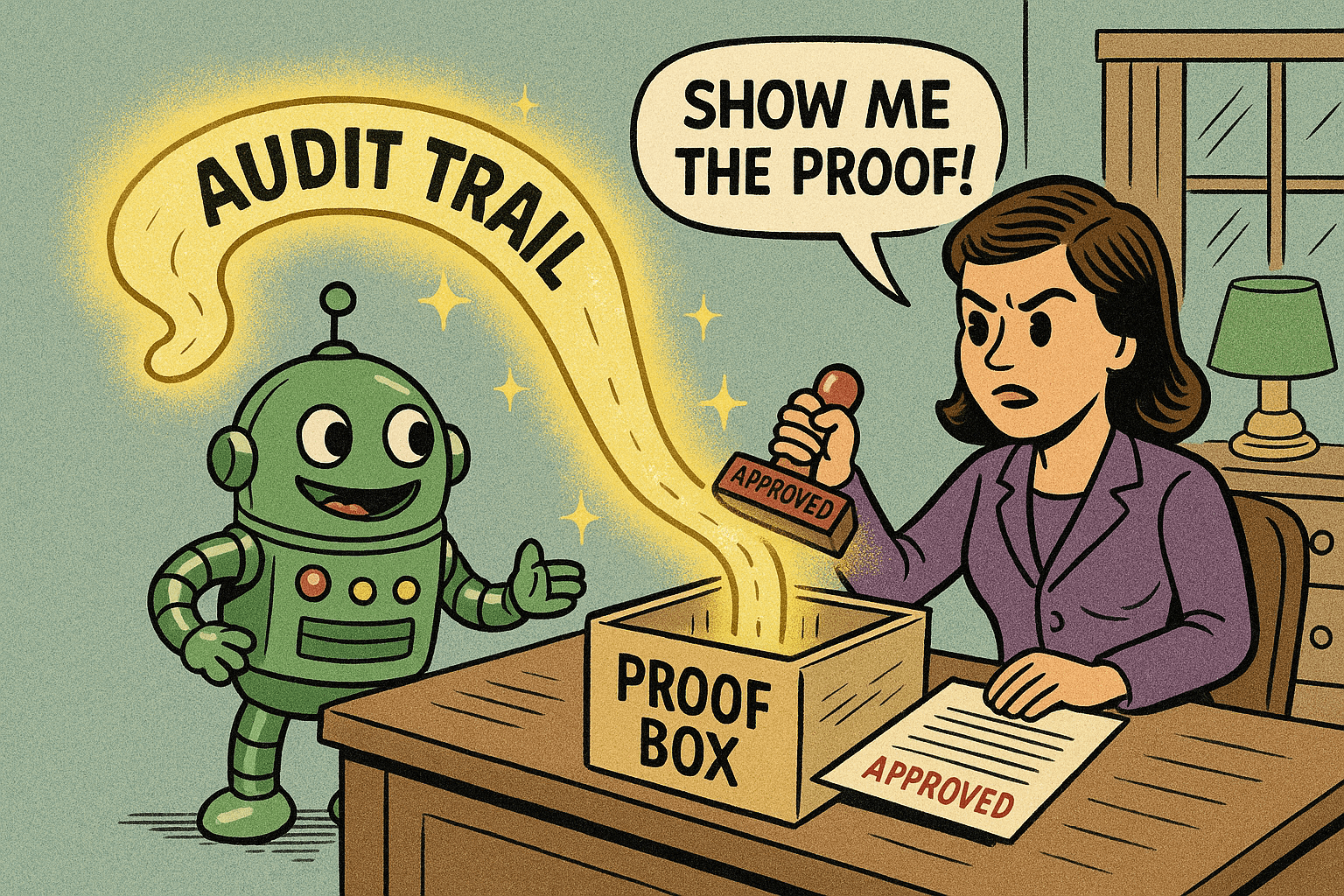

The biggest operational risk when claiming a business bad debt deduction is not the accounting method, but the lack of clear, complete documentation of collection attempts.In manual collections environments, call logs and email histories are often disorganized, incomplete, or impossible to retrieve years later during an audit. Modern AR automation platforms solve this fundamental compliance problem.

Leveraging Automation to Simplify AR Cleanup and Tax Preparation

AI-powered collection platforms are inherently designed with compliance as a core function. They automatically create a complete, standardized, and time-stamped audit trail of every single communication, whether that is a personalized email or a conversation managed by an AI calling agent. This automated documentation transforms the process of IRS compliance from a manual risk into a guaranteed feature, providing the exact evidence needed to prove that "documented efforts to collect the debt were made. This automated audit trail is invaluable for substantiating tax season receivables deductions.

The value of automation extends far beyond documentation. Companies that implement AR automation solutions typically report a measurable decrease in bad debt write-offs, often in the range of 10% to 15%. This reduction occurs because automated workflows flag and manage at-risk accounts much earlier, preventing potential problems from escalating into uncollectible debts.

This operational efficiency frees finance teams from the tactical burden of manual chasing, allowing them to focus on the high-level, strategic tasks critical for year-end success, such as complex negotiations and detailed AR reconciliation. For service-based SMBs and startups that rely heavily on invoicing, including trades, medical clinics, and professional firms, AI platforms like Abivo integrate seamlessly with common accounting platforms, such as QuickBooks, NetSuite, Xero, and SAP Business One, to make this high-level, compliant automated AR cleanup accessible and effective.

Your Actionable Checklist for a Stronger Financial Close

When approaching the final days of the fiscal year, use these key action items to ensure a clean closing process:

Prioritize Immediate Action: Focus all remaining, targeted collection effort on accounts currently sitting in the 61–90 day and 90+ day aging buckets, as these accounts represent the highest risk to year-end cash flow.

Balance the Books: Run and reconcile your AR subsidiary ledger against the General Ledger to ensure accurate end-of-year totals and resolve any posting or adjustment errors immediately.

Clear the Clutter: Proactively resolve all unapplied credits, customer prepayments, and outstanding credit balances to eliminate discrepancies that distort your true AR position.

Automate Your Final Push: Leverage AI communication tools to send documented, compliant, and timely final reminders via call and email, optimizing the recovery of tax season receivables before cutoff.

Document Worthlessness: Before formally writing off any debt, ensure your automated system has generated the mandatory audit trail of collection attempts needed for IRS compliance.

Consult Your CPA: Always confirm the correct bad debt accounting method, especially if you use a cash basis, and ensure you use the proper tax reporting forms (e.g., Schedule C or Form 1120-S) for your specific business entity.

Beyond the Close: Setting the Stage for Future Growth

Mastering the year-end AR process is fundamentally about more than just recovering old debt; it is about establishing a clear, accurate, and compliant foundation for the upcoming year. A systematic cleanup ensures better cash flow management, maximizes legitimate deductions related to tax season receivables, and provides management with the accurate financial forecasting data necessary for smart decision-making.

By adopting this methodical approach, integrating meticulous AR reconciliation with strategic collections and strict compliance documentation, finance leaders can move beyond the year-end scramble. Leveraging tools that automate AR cleanup means that critical tasks like documentation and follow-up are handled consistently and compliantly, allowing human professionals to focus on strategy and negotiation. This deliberate move toward efficiency and accuracy empowers businesses to start the new fiscal year not in a state of chaos, but with financial clarity and strategic confidence.