Credit Agreements 101: What to Include When Extending Terms

Essential protections to safeguard your right to collect and maintain cash flow

Sia Ghazvinian

Co-Founder & CEO

Table of contents

Share

Extending Credit Is a Growth Lever, and a Risk

Offering credit terms is often the key to winning bigger deals, smoothing procurement, and building long-term relationships, especially in professional services. But it comes with exposure. Unlike product-based businesses that can reclaim goods, service providers often deliver intangible value before payment, heightening the risk.

Across North America, the risk is tangible: nearly 45% of B2B invoices in the U.S. and over 60% in Canada are paid late. That delay drains working capital, stalls reinvestment, and forces teams to chase revenue already earned.

Modern credit agreements need to move beyond legacy boilerplate. They must protect, predict, and guide, anchoring financial health while signaling professionalism to the client.

Legal Clauses That Guide Behavior, Not Just Enforce It

Adaptive Terms That Reflect Relationship Health

The best agreements evolve with your customer. Fixed terms like "Net 30" treat a startup and an enterprise buyer the same, which rarely makes sense. Instead, structure dynamic terms that adjust to payment history, creditworthiness, or order volume.

For example:

Start all clients on Net 15 with clear onboarding expectations.

Automatically extend to Net 30 after three on-time payments.

Offer Net 45 terms only if supported by trade insurance or collateral.

This creates a system that rewards reliability while limiting blind exposure. It also gives your finance team more leverage to reset terms if patterns shift.

Tiered Late Fees to Create Time-Based Urgency

A single late fee can be ignored. A progressively escalating structure builds pressure while still staying within regulatory bounds. For example:

"A 1% monthly charge applies after 30 days; 1.5% applies after 60 days; the maximum charge shall not exceed applicable provincial or state interest limits."

While usury laws vary by jurisdiction, a tiered model motivates earlier resolution without relying solely on final demand letters.

Credit Triggers That Prevent Silent Risk

Defaults rarely happen in isolation. They’re usually preceded by subtle red flags: slowing payments, management changes, or operational strain. A good agreement creates automated checkpoints that kick in before a major delinquency.

Useful language might include:

"If any invoice exceeds 45 days past due, all future deliveries may be suspended pending credit review."

"The Company may request updated financial disclosures in the event of layoffs, material adverse events, or public credit downgrades."

This structure lets your team pause risk before the situation escalates.

Drafting for Influence: Using Psychology to Get Paid Faster

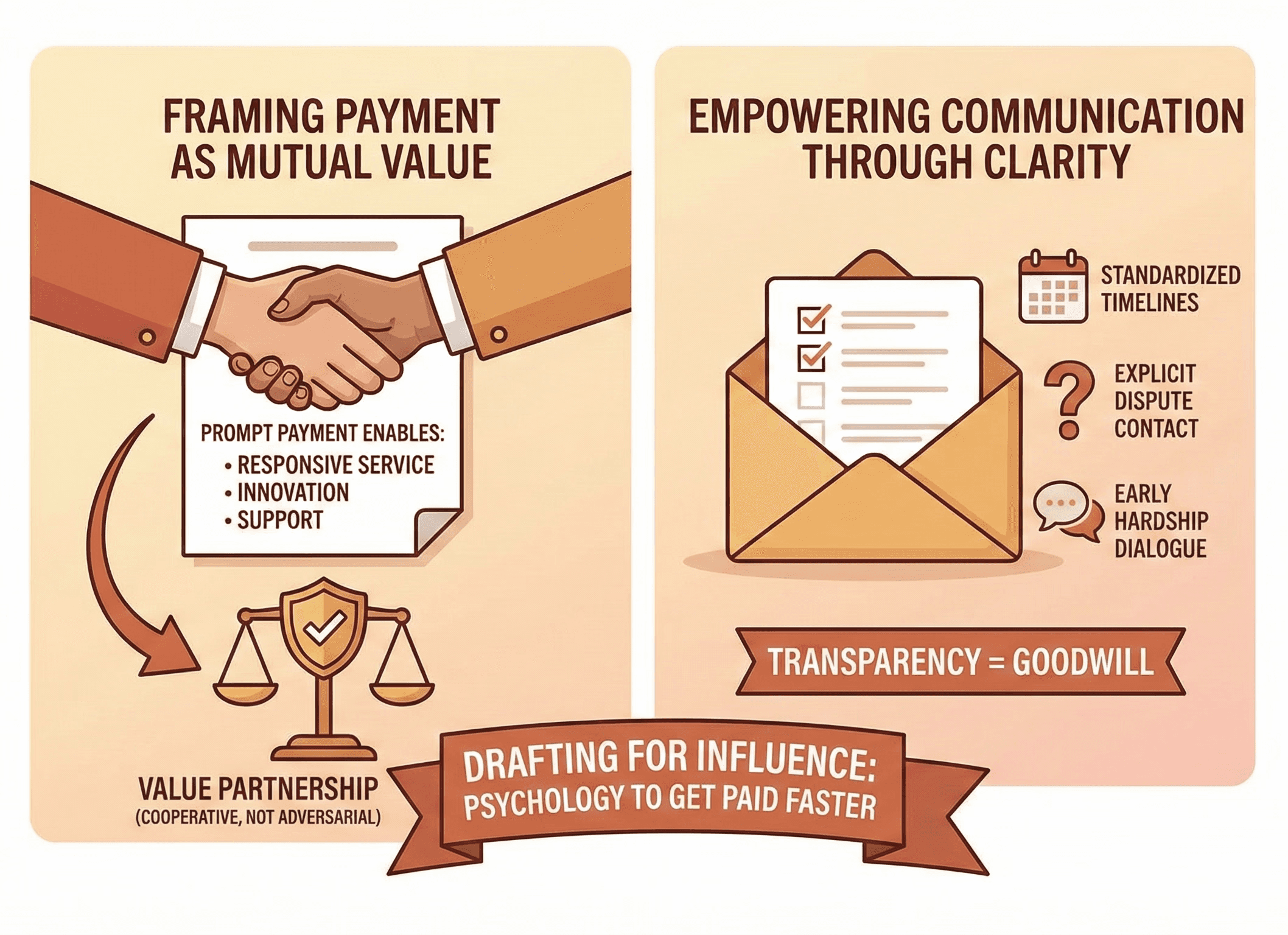

Language That Frames Payment as Mutual Value

Behavioral economists have shown that people respond better to agreements that feel cooperative, not adversarial. Use language that emphasizes shared benefit:

"Prompt payment enables us to maintain responsive service levels, invest in innovation, and continue supporting your growth."

This approach reduces defensiveness, and positions your terms as part of a value partnership—not a trap.

Empowering Communication Through Clarity

A common reason for late payment is simple confusion. Clarity reduces friction. Consider:

Standardized billing timelines (e.g. "Invoices issued on the 1st for that month’s services.")

Explicit contact procedures for disputes ("Disputes must be raised within 7 business days.")

Invitation language for hardship plans ("Please contact our team in advance if you foresee payment difficulty; we may offer structured extensions.")

This encourages transparency early, and builds goodwill even when payments are delayed.

U.S. vs. Canada: Structuring for Cross-Border Confidence

Operating across jurisdictions means understanding both the legal and cultural landscape. Some key differences:

In Canada

To enforce security interests (i.e. collateral), agreements must often align with PPSA rules and may require provincial filings.

In Quebec, French-language contracts are mandatory for many business relationships.

Early-payment incentives should avoid triggering scrutiny under provincial anti-kickback regulations.

In the U.S.

Interest rates and penalty clauses must comply with state-level usury laws. A clause legal in Delaware may not hold in California.

If collateral is involved, you’ll likely need to file a UCC-1 to establish priority over other creditors.

Government contracts, medical billing, or educational services may be subject to additional billing guidelines under federal or sector-specific statutes.

A strong agreement includes a governing law clause and specifies which court (or arbitration body) will resolve disputes.

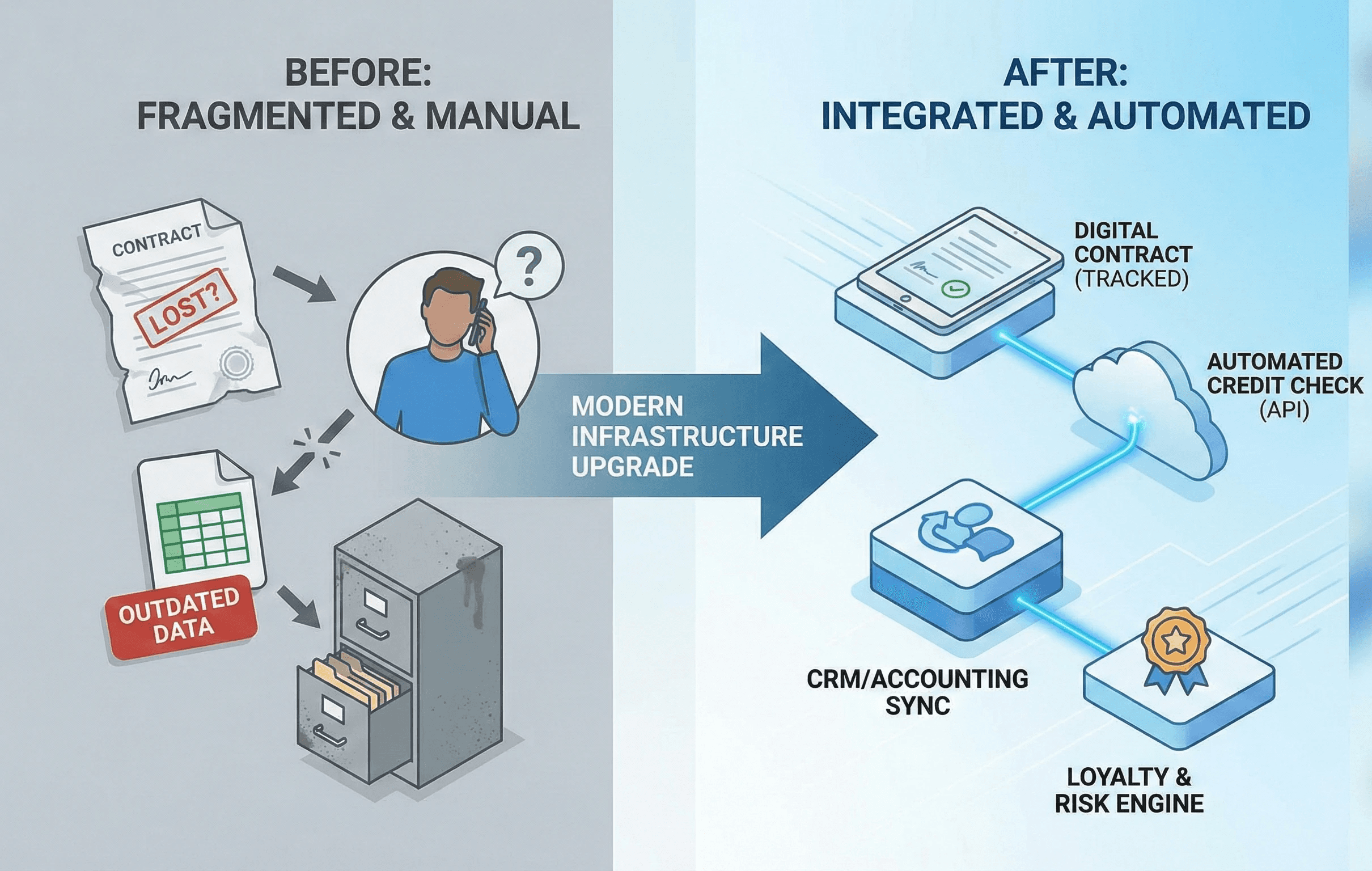

Operationalizing Credit Agreements With Modern Infrastructure

Use Digital Contracts with Version Tracking

Static PDFs or emailed Word docs make it easy for terms to get lost, or disputed. Instead, use a contract platform that:

Tracks acceptance by timestamp and IP

Integrates with CRM or accounting systems for future lookup

Flags agreements nearing expiry or lacking renewal

This ensures you’re not operating on assumptions, or outdated terms.

Automate Credit Assessment Into the Application

A growing number of finance teams are embedding automated scoring into their onboarding workflow. Services like credit API providers let you:

Instantly check public lien or bankruptcy databases

Pull trade history from partners (with permission)

Set real-time risk flags when payment patterns change

Combined with flexible terms and clear agreement clauses, this creates a complete credit intelligence stack.

Rewarding Behavior Through Agreement-Based Loyalty

Some businesses now include behavior-based rewards in their agreements. Instead of discounts applied ad hoc, they formalize recognition:

"Clients who maintain 100% on-time payment over any 12-month period will be eligible for priority scheduling, early access to services, or bonus consulting hours."

When tied to milestones, these rewards encourage accountability and reduce the need for separate loyalty programs.

A Strategic Credit Agreement Sets the Tone

This isn’t just legal protection. A good credit agreement is a signal, it tells your client:

You take cash flow seriously

You’ve thought about how to manage risk collaboratively

You reward partnership, not just penalize lapses

By combining behavioral science, legal foresight, and modern digital tools, service-based businesses can turn credit terms into a lever for trust and financial resilience.