How Inflation and Interest Rates Impact Accounts Receivable and What You Can Do About It

Inflation and rising rates can delay payments and reduce cash value. Smart AR practices and automation help protect cash flow.

Sia Ghazvinian

Co-Founder & CEO

Table of contents

Share

Inflation and rising interest rates may seem like macroeconomic concepts far removed from your day-to-day work in accounts receivable (AR), but they have real effects on how customers pay invoices and how quickly businesses receive cash. When prices climb and borrowing costs go up, both you and your customers feel the squeeze. That can change payment behavior, increase cash flow risk, and make effective AR management more important than ever.

In this article you’ll learn how inflation and interest rates influence AR outcomes, why delays and aging receivables worsen in tough economic times, and what businesses can do to protect cash flow and maintain healthier financial operations.

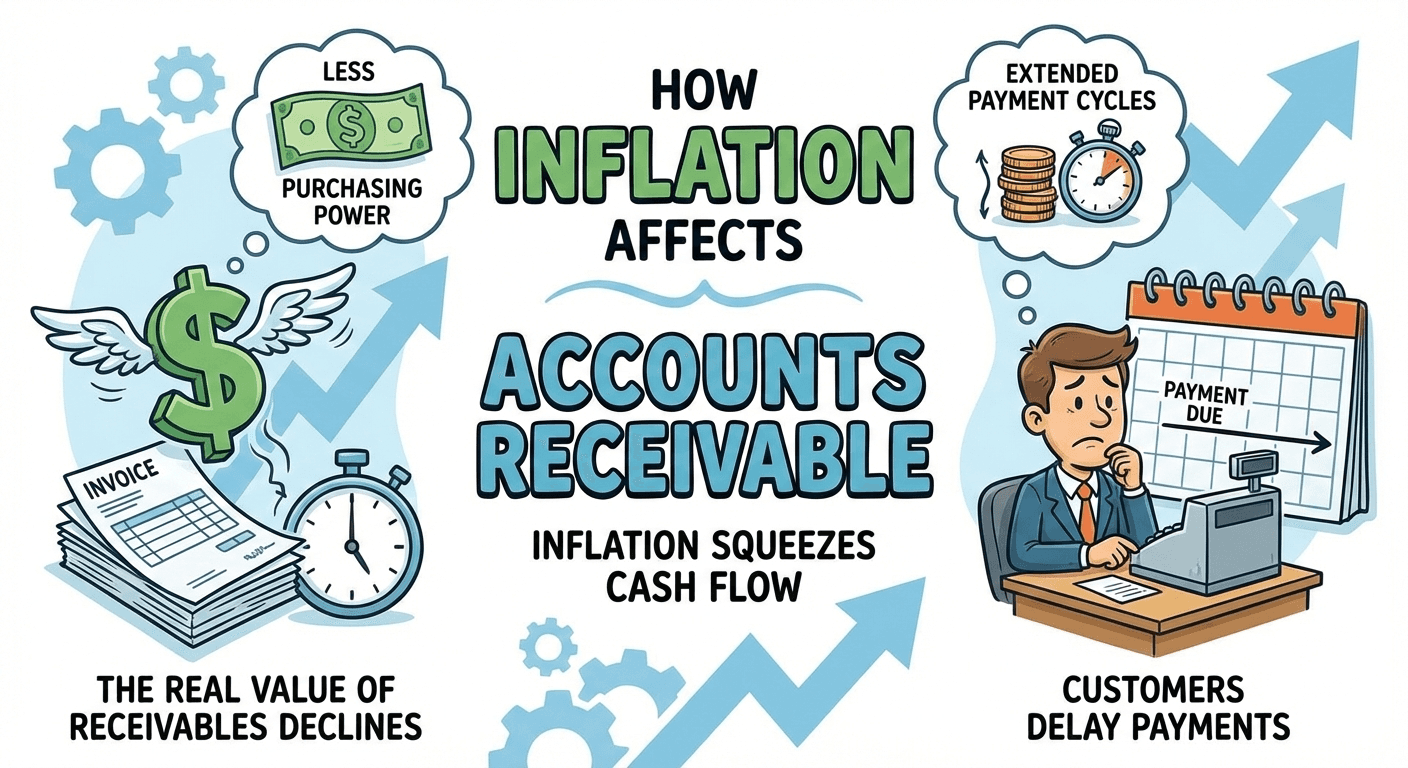

How Inflation Affects Accounts Receivable

Inflation means that the value of currency declines over time: today’s dollar buys less than it did yesterday.

For accounts receivable, this has two key implications.

1. The Real Value of Receivables Declines

When you issue an invoice today and it isn’t paid for 30 or 60 days, the money you eventually collect is worth less in real terms than when the work was done or the product delivered. This effect worsens in high-inflation periods. Every day that passes before collection reduces the purchasing power of that cash.

For example, if your customer pays a 30-day invoice late in a high-inflation environment, the dollars you receive buy less than they would have at the time of invoicing. In effect, inflation acts like an implicit negative interest on your receivables.

2. Customers Delay Payments to Preserve Their Cash

Inflation squeezes budgets at every level of the economy. Your customers are also facing higher costs for supplies, wages, and debt servicing, which often leads them to extend their payment cycles to manage their own cash flow. Research and practitioner observations note that in inflationary environments businesses often see customers take longer to pay, increasing days sales outstanding (DSO) and delinquencies.

Late payments not only delay your cash inflows, they also make your AR aging profile worse, raising the risk of bad debts or write-offs.

Rising Interest Rates and Customer Behavior

Central banks raise interest rates to control inflation. While this may eventually stabilize prices, in the short term it creates its own challenges for cash flow and AR.

Higher Borrowing Costs for Businesses

When interest rates rise, borrowing becomes more expensive for companies of all sizes. That affects your customers if they rely on lines of credit or loans to finance operations or pay suppliers. Higher borrowing costs reduce available liquidity, so some customers stretch out payables to preserve cash, including payments to your business.

Tightening AR Financing Conditions

If you use accounts receivable financing (selling or borrowing against invoices), rising interest rates typically mean discount rates and borrowing costs go up and lenders tighten credit standards. That can make financing receivables less attractive or more costly, reducing another tool businesses often use to smooth cash flow.

Indirect Effect on Customer Demand

Higher interest rates also reduce borrowing and spending across the economy. Customers may delay or scale back purchases or projects, reducing future billing and potentially delaying payments already owed. This, in turn, affects your pipeline of new business and the pace at which receivables turn into cash.

The Combined Effect: Slower, Less Valuable Payments

Inflation and rising interest rates often occur together, creating a “perfect storm” for AR:

Invoices lose value over time, eroding real cash inflows.

Customers delay payment due to cash constraints.

Financing receivables gets more expensive or restricted.

Collections activities become more intense and necessary to maintain liquidity.

All of these trends blend into slower collections, higher DSO, and greater pressure on working capital.

What Businesses Can Do to Protect Cash Flow

Facing inflation and a rising rate environment doesn’t mean your AR has to deteriorate uncontrollably. Here are practical steps to help safeguard your receivables and cash flow.

1. Monitor Receivables Aging Actively

Closely tracking your AR aging and DSO is essential. When macroeconomic pressures increase, trends can shift quickly, and early detection of slowing payments helps you act before balances become uncollectible. Over 80 percent of invoices were paid late during high-inflation periods in recent years, highlighting the importance of monitoring aging closely.

2. Tighten Credit Policies

Reassess how much credit you extend and to whom. Tightening terms for customers with weaker payment histories or shorter credit windows reduces your exposure. Clear credit policies also send a strong signal to customers about expectations.

3. Offer Incentives for Early Payment

Dynamic discounting (offering a small discount for paying early) is a strategy that accelerates collections and improves liquidity while giving customers a financial reason to pay sooner. Often, the cost of the discount is less than the cost of delayed cash flow.

4. Encourage Multiple Payment Options

Providing easy and modern payment methods (credit card, ACH, digital wallets) reduces friction and can lead to faster collections. The simpler it is for customers to pay, the less likely they are to postpone payment.

5. Consider Receivables Financing Strategically

In high-rate environments, standard borrowing costs rise, but invoice factoring or similar financing can offer a way to unlock cash tied up in receivables without traditional debt financing, helping maintain liquidity through uncertain periods.

6. Leverage Automation for Consistency

Automation ensures invoices and follow-up reminders are sent according to schedule, reducing manual errors and inconsistency, critical factors in maintaining collections momentum.

The Strategic Importance of AR in Economic Shifts

Inflation and higher interest rates are more than economic headlines. They shape customer behavior, financial risk, and the operational realities of accounts receivable. In tough economic climates, AR teams that act proactively, tightening terms, using incentives wisely, and embracing digital tools, are better positioned to protect cash flow and maintain financial health.

While you cannot control macroeconomic conditions, you can influence how resilient your receivables process is in the face of them.

Practical Takeaways

Inflation erodes the real value of receivables, making timely collection more important than ever.

Customers may delay payments when faced with higher costs and borrowing rates.

Rising interest rates increase borrowing costs for businesses and can tighten AR financing options.

Actively monitor aging, tighten credit policies, and use incentives to encourage faster payments.

Modern payment options and automation make it easier for customers to pay well before terms expire.