The Global Collections Playbook

A comprehensive guide for finance leaders on mastering cross-border accounts receivable. Learn to navigate VAT rules, e-invoicing mandates, and currency risks while leveraging automation to secure revenue.

Pratheek Adi

Co-Founder & CTO

Table of contents

Share

The Silent Friction in Global Growth

For service-based businesses, the allure of the global market is undeniable. The digital economy has lowered the barriers to entry, allowing a marketing agency in Austin to serve clients in London, or a software development firm in Toronto to partner with enterprises in Berlin. However, this expansion brings a silent friction that often goes unnoticed until it threatens the very liquidity of the organization. This friction is not a lack of demand or a failure of service delivery, but the sheer, overwhelming complexity of getting paid across borders.

Recent data paints a stark picture of the accounts receivable landscape. In the United States, 55% of all B2B invoiced sales are currently overdue. This is not merely a symptom of lazy payers; it is a structural failure in the invoicing process. When a business steps outside its domestic borders, it enters a labyrinth of conflicting regulations, tax mandates, and banking protocols. A simple error, such as a missing VAT identification number or an incorrect currency code, can cause an invoice to be rejected instantly by a client’s automated accounts payable system or blocked by a foreign government’s tax portal.

The consequences of these errors are severe. Invoice rejections have surged by 273% in early 2025, driven by trade uncertainty and the increasing automation of compliance checks. For a business operating on net payment terms, a rejection effectively resets the clock. A Net-30 invoice rejected on day 25 becomes a Net-60 or Net-90 liability, tying up working capital that is desperate needed for payroll and growth.

This report serves as a definitive guide for finance professionals and business owners navigating this complexity. We will dissect the shifting regulatory sands of global e-invoicing, explore the financial mechanics of cross-border collections, and demonstrate how automation platforms like Abivo are transforming accounts receivable from a back-office burden into a strategic asset.

The Paradigm Shift in Global Taxation

To understand how to comply, one must first understand why the rules are changing. For decades, global taxation operated on a "post-audit" model. Businesses issued invoices, collected taxes, and filed returns. Tax authorities would review these records months or years later. This system relied heavily on trust and created massive opportunities for error and fraud.

The "VAT Gap", the difference between the expected VAT revenue and the amount actually collected, reached staggering levels, estimated at €61 billion in the European Union alone in 2021. In response, governments are abandoning the post-audit model in favor of Continuous Transaction Controls (CTC).

The Rise of the Clearance Model

Under a CTC or "clearance" model, the tax authority inserts itself directly into the transaction flow. An invoice is no longer a private document between supplier and buyer. Instead, the invoice data must be sent to, validated by, and "cleared" by the government's tax platform before it can be legally issued to the customer.

If the data is incorrect, if a mandatory field is missing, or a tax calculation does not match the regulated schema, the government platform rejects the invoice immediately. It effectively does not exist in the eyes of the law until it is corrected. This shift transforms invoicing from a simple administrative task into a high-stakes compliance activity where accuracy is paramount.

VAT in the Digital Age (ViDA)

The European Union is spearheading this global transformation through its VAT in the Digital Age (ViDA) initiative. Adopted to modernize the VAT system for the 21st century, ViDA introduces strict new requirements that impact any business trading with or within the EU.

The initiative is built on three central pillars that redefine compliance:

Digital Reporting Requirements (DRR): This mandate requires businesses to submit data on cross-border transactions to national tax administrations in near real-time. The days of summarizing transactions in a monthly report are ending. Data must be granular, transactional, and immediate.

The Platform Economy: New rules clarify that digital platforms facilitating sales (such as gig economy apps or marketplaces) are responsible for collecting and remitting VAT. This levels the playing field between traditional providers and digital disruptors.

Single VAT Registration: ViDA expands the One Stop Shop (OSS) mechanism, allowing businesses to register for VAT in a single Member State and sell across the entire EU without multiple registrations. This is a significant simplification for US businesses selling digital services to European consumers.

For US-based SMBs, ViDA is a signal that the "wild west" of cross-border digital trade is closing. Your European clients will increasingly demand invoices that comply with these rigorous standards because they need compliant invoices to reclaim their own taxes.

The Global E-Invoicing Mandate Tracker

While the EU provides a directive, individual countries are implementing their own specific mandates on different timelines. A "one-size-fits-all" invoice template is a recipe for rejection. Businesses must be aware of the specific requirements in their key export markets.

Europe: The Epicenter of Change

Europe is currently the most active region for regulatory change, driven by the need to harmonize standards across the single market.

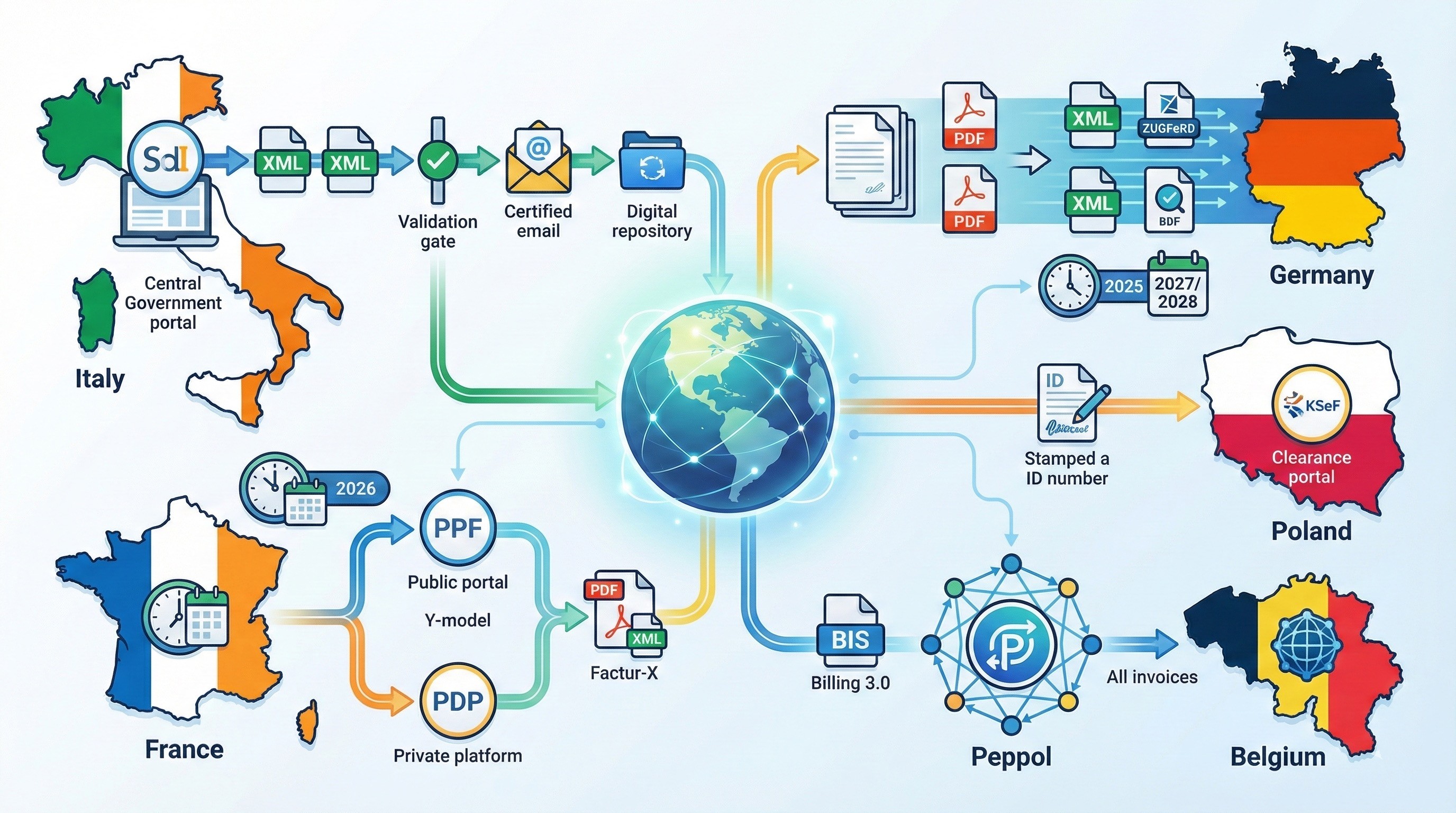

Italy: The Pioneer of Control

Italy was the first EU country to mandate generalized B2B e-invoicing, setting the template for others to follow.

The System: Sistema di Interscambio (SdI).

The Requirement: All invoices (B2B, B2G, and B2C) must be transmitted to the SdI portal in the FatturaPA XML format.

The Process: The supplier generates the XML file and sends it to SdI. The SdI system automatically validates the file against technical rules. If valid, SdI delivers the invoice to the customer’s certified email address or digital repository. If the invoice bypasses SdI (e.g., sent via PDF email), it is considered legally non-existent, and hefty penalties apply.

Implication for US Businesses: While non-resident businesses were historically exempt, cross-border transactions must now be reported. US businesses billing Italian clients should expect requests for structured data to help their clients comply with "Esterometro" (cross-border) reporting rules.

France: The Upcoming Giant

France is rolling out a comprehensive B2B e-invoicing mandate starting in 2026, utilizing a "Y-model" that gives businesses a choice of platforms.

Timeline:

September 2026: Obligation to receive e-invoices applies to all businesses. Large and mid-sized enterprises must also issue e-invoices.

September 2027: Small and medium enterprises (SMEs) and micro-businesses must issue e-invoices.

The Architecture: Businesses can choose to connect to the public portal (PPF) or use a certified private platform (PDP).

Formats: France accepts UBL, CII, and the innovative Factur-X format. Factur-X is a hybrid: a human-readable PDF file that contains an embedded XML data file. This allows automation systems to read the data while humans can still read the document.

Germany: The Awakening Giant

Germany has traditionally relied on paper and standard PDFs, but the Wachstumschancengesetz (Growth Opportunities Act) is forcing a rapid digital transition.

Timeline:

January 2025: All German businesses must be able to receive and process e-invoices.

January 2027/2028: Mandatory issuance of e-invoices will be phased in based on company turnover.

Formats: The standard is ZUGFeRD (compatible with Factur-X) and XRechnung (pure XML). The era of sending a simple Word document saved as a PDF is ending in Germany's B2B sector.

Poland: Centralized Clearance

Poland is implementing the National System of e-Invoices (KSeF), moving to a centralized clearance model similar to Italy.

Mandate: Mandatory B2B e-invoicing is scheduled for 2026 (delayed from an initial 2024 target).

Format: FA_VAT XML.

Mechanism: Invoices are sent to KSeF, validated, and assigned a unique KSeF ID number. This number is required for the invoice to be valid. For foreign businesses with a fixed establishment in Poland, this system is mandatory.

Belgium: Peppol First

Belgium has taken a decisive step toward standardization by mandating the Peppol network.

Timeline: Mandatory B2B e-invoicing starts January 1, 2026.

Standard: All invoices must be exchanged via the Peppol network using the Peppol BIS Billing 3.0 format. This eliminates the need for proprietary portals and aligns Belgium with the broader European interoperability framework.

The Peppol Network: A Global Standard

As countries roll out these mandates, a common infrastructure is emerging to prevent fragmentation: Peppol (Pan-European Public Procurement On-Line). Despite the name, it is now a global standard used in Singapore, Australia, New Zealand, and Japan.

Peppol is not a platform you log into; it is a delivery network, similar to the telecom network. You connect to it via a certified Access Point. It uses a "4-corner model" to ensure secure delivery:

Corner 1 (You): You send the invoice to your Service Provider.

Corner 2 (Your Access Point): Your provider validates the invoice against the standard (Peppol BIS 3.0) and sends it.

Corner 3 (Client's Access Point): The client's provider receives the invoice.

Corner 4 (The Client): The client receives the invoice directly into their ERP or accounting software.

For US businesses using major ERPs like NetSuite or Microsoft Dynamics, connecting to a Peppol Access Point is often the most efficient way to ensure compliance across multiple regions without building custom integrations for each country.

Asia-Pacific and Latin America

While Europe focuses on interoperability, other regions have their own distinct models.

Latin America: Countries like Brazil, Chile, and Mexico were the global pioneers of e-invoicing. They use strict clearance models where invoices must be digitally signed and approved by the tax authority (e.g., SAT in Mexico) before goods can even be shipped. Real-time reporting is the norm here.

Asia-Pacific: Singapore, Australia, and New Zealand have adopted the Peppol framework to facilitate cross-border trade, though it remains largely voluntary for B2B transactions currently. However, Japan is introducing the "Qualified Invoice System" (similar to VAT invoices) which is pushing businesses toward digital adoption.

Overview of Key Mandates

Country | Mandate Status | Key System/Format | Implementation Date |

Italy | Mandatory (B2B, B2G) | SdI (FatturaPA) | Active |

France | Mandatory (Phased) | PDP/PPF (Factur-X) | Sept 2026 (Large/Mid) |

Germany | Mandatory (Receive) | ZUGFeRD, XRechnung | Jan 2025 (Receive) |

Poland | Mandatory (B2B) | KSeF (FA_VAT) | Feb 2026 |

Belgium | Mandatory (B2B) | Peppol BIS 3.0 | Jan 2026 |

Romania | Mandatory (B2B) | RO e-Factura | Jan 2024 |

Spain | Planned (B2B) | VeriFactu | Pending (Est. 2025/26) |

Malaysia | Phased Rollout | LHDN (Peppol) | Aug 2024 (Large) |

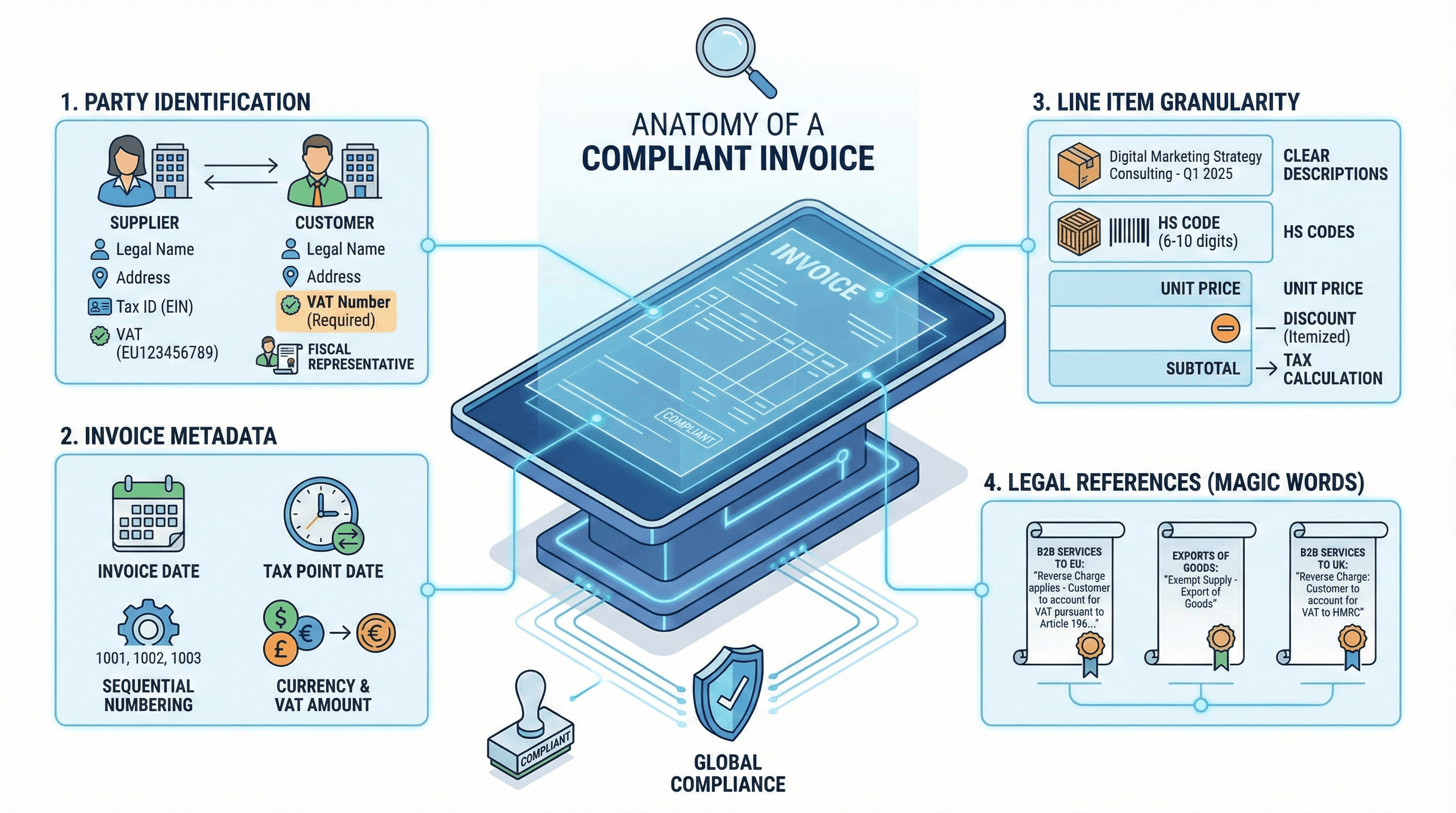

The Anatomy of a Compliant Invoice

In the domestic US market, an invoice can often be a simple PDF generated by QuickBooks with basic details: "Consulting Services - $5,000." In the international arena, such an invoice is a liability. It lacks the data granularity required for customs, tax determination, and automated processing.

To ensure your invoices flow smoothly through your client's accounts payable systems and government portals, you must adhere to strict data standards.

1. Party Identification

Ambiguity is the enemy of compliance. You must clearly identify who is selling and who is buying.

Supplier Details: Your invoice must list your full legal name, registered address, and your tax identification number. For US businesses, this is your EIN. If you are registered for VAT in the EU (via OSS, for example), you must include that VAT number (e.g., EU123456789).

Customer Details: You must list the customer's full legal name and address. Crucially, you must include the Customer's VAT Number. This is the single most important field for B2B cross-border transactions in Europe. It triggers the "Reverse Charge" mechanism (discussed in Part IV). If this number is missing or incorrect, you may be held liable for the VAT.

Fiscal Representative: If your business is required to appoint a fiscal representative in a specific country (common for non-EU importers), their name, address, and tax ID must also appear on the invoice.

2. Invoice Metadata

These fields establish the legal timeline and uniqueness of the document.

Sequential Numbering: Invoices must have a unique, sequential number. Gaps in the sequence (e.g., jumping from Invoice #1001 to #1005) are red flags for tax auditors in countries like France and Italy, suggesting missing revenue.

Dates: You should include two dates: the Invoice Date (when the document was created) and the Tax Point Date (or Time of Supply), which is when the service was performed or payment received. This distinction is vital because the Tax Point determines the exchange rate used for VAT calculations.

Currency: You can invoice in any currency (USD, EUR, GBP), but if VAT is applicable, the VAT amount must usually be expressed in the local currency of the customer's country, using the official central bank exchange rate for the tax point date.

3. Line Item Granularity

Vague descriptions are a primary cause of invoice rejection.

Clear Descriptions: Instead of "Marketing Services," use "Digital Marketing Strategy Consulting - Q1 2025."

HS Codes: For businesses shipping physical goods, the Harmonized System (HS) code is mandatory. This 6-to-10 digit code tells customs authorities exactly what the product is, determining duties and tariffs. An incorrect HS code can lead to goods being held at the border and the invoice remaining unpaid.

Unit Price and Discounts: Discounts should not be lumped into a final total. They must be itemized or clearly applied to the subtotal before any tax calculation.

4. Legal References (The "Magic Words")

If you are not charging VAT (which is common for exports), you cannot simply leave the tax line blank or at $0.00. You must include a legal reference explaining why.

For B2B Services to EU: "Reverse Charge applies - Customer to account for VAT pursuant to Article 196 of Council Directive 2006/112/EC".

For Exports of Goods: "Exempt Supply - Export of Goods".

For B2B Services to UK: "Reverse Charge: Customer to account for VAT to HMRC".

Failure to include these specific phrases can render the invoice invalid, preventing your client from justifying the lack of tax to their authorities.

Navigating the Tax Maze (VAT & GST)

The concept of Value Added Tax (VAT) is often foreign to US businesses accustomed to Sales Tax. Sales Tax is a one-time levy at the point of purchase. VAT is a multi-stage tax collected at every step of production. When you sell internationally, you are entering this VAT ecosystem.

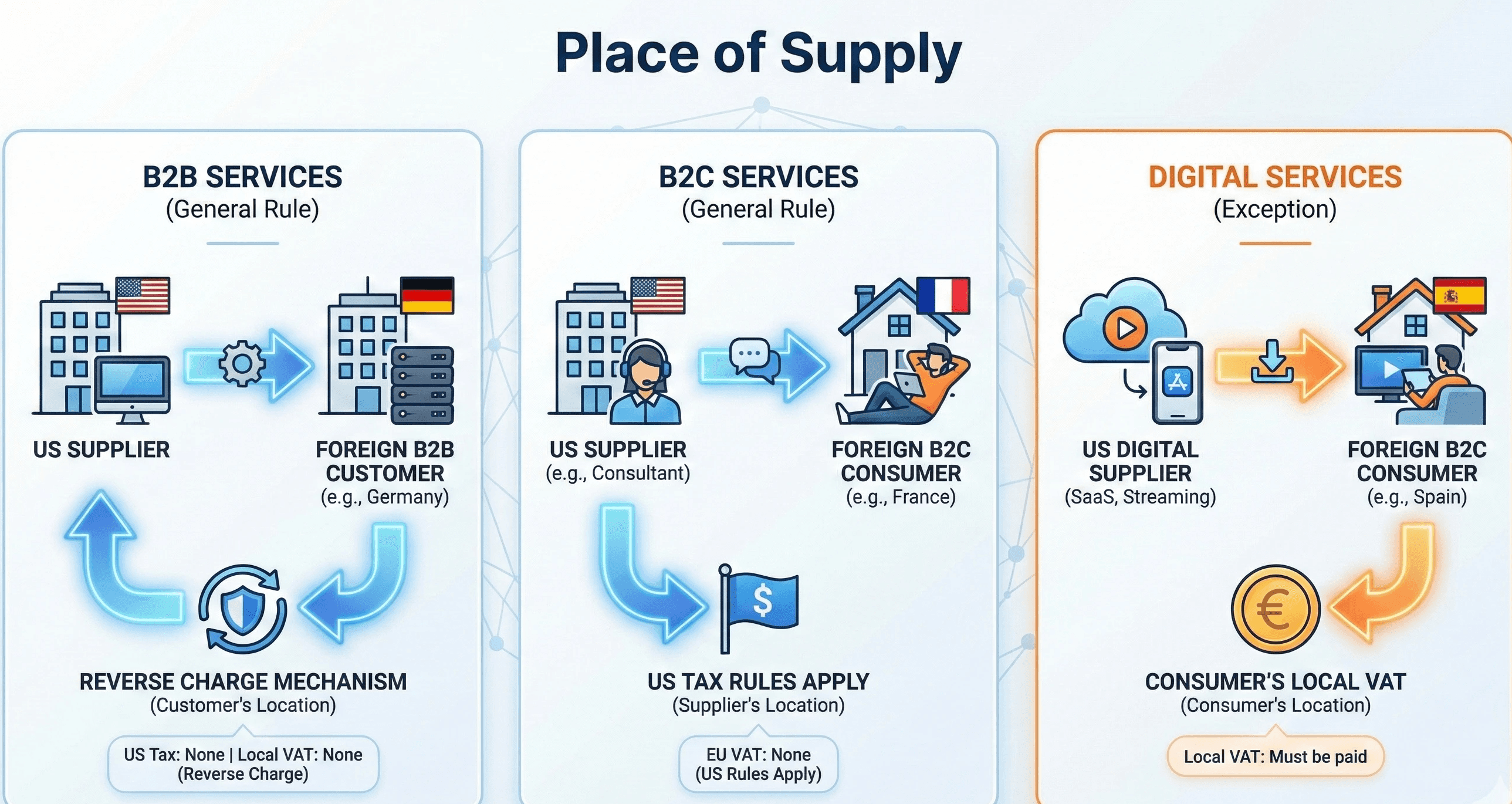

The Place of Supply Rules

To determine if you need to charge tax, you must determine the "Place of Supply." This legal concept dictates which country has the right to tax the transaction.

The General Rule for B2B Services

When a business sells services to another business (B2B), the place of supply is generally where the customer is established.

Scenario: A US design agency invoices a German software company.

Result: The place of supply is Germany.

Action: The US agency does not charge US Sales Tax. They also do not typically charge German VAT. Instead, they apply the Reverse Charge Mechanism.

The General Rule for B2C Services

When a business sells services to a consumer (B2C), the place of supply is generally where the supplier is established.

Scenario: A US consultant advises a private individual in France.

Result: The place of supply is the US.

Action: No EU VAT is charged (though US tax rules may apply).

The Critical Exception: Digital Services

For "electronically supplied services" (streaming, software downloads, e-books, SaaS), the rule flips. The place of supply is where the consumer is located, regardless of B2B or B2C status.

Scenario: A US SaaS company sells a subscription to a user in Spain.

Result: The place of supply is Spain. Spanish VAT must be paid.

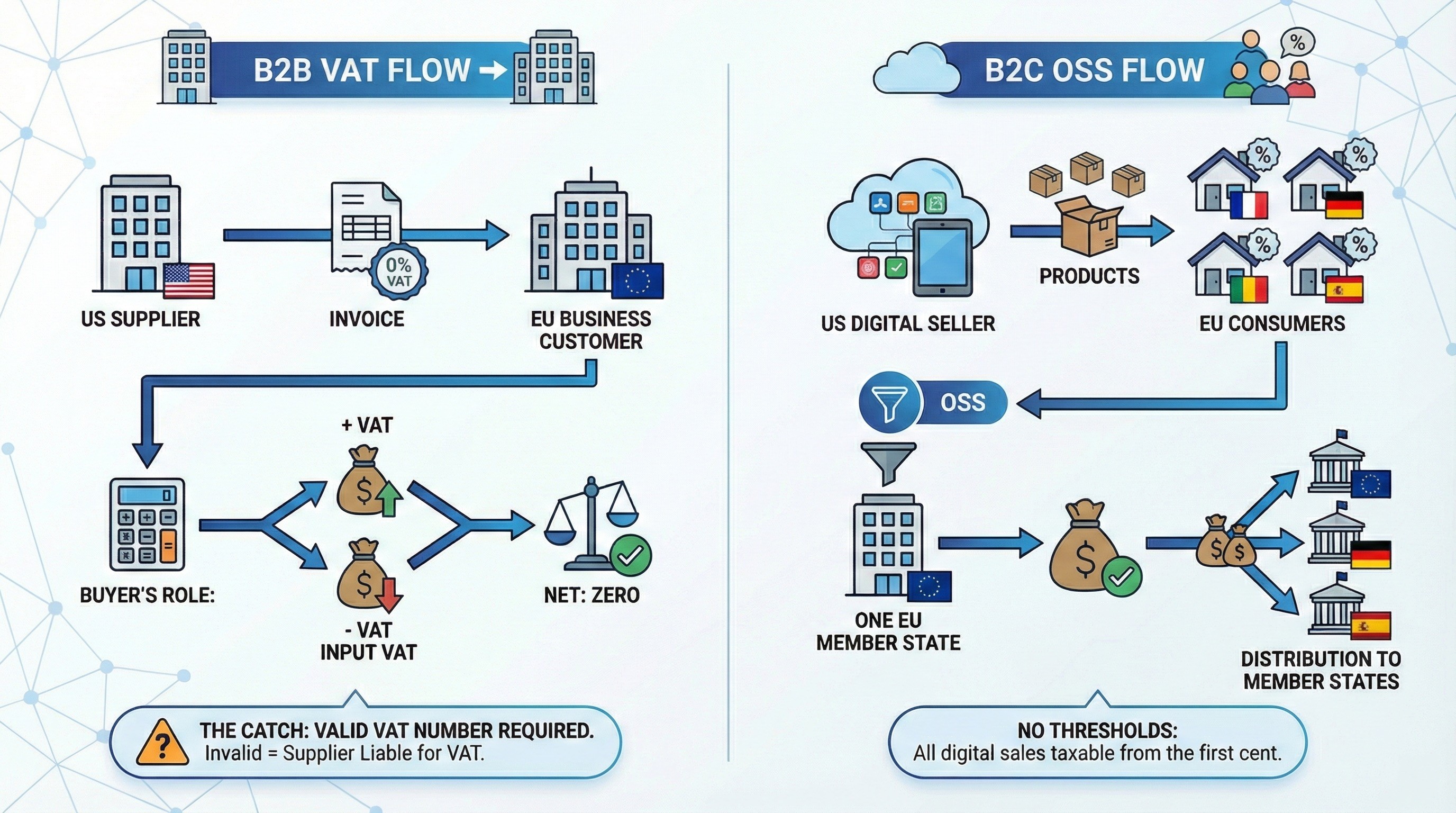

The Reverse Charge Mechanism: A B2B Lifeline

The Reverse Charge is the mechanism that keeps global B2B trade flowing without requiring every supplier to register for tax in every country. It shifts the tax responsibility from the seller to the buyer.

How it Works: You issue an invoice for €1,000 with 0% VAT. You mark it as "Reverse Charge."

The Buyer's Role: Your customer in Europe receives the invoice. In their own tax return, they report a "virtual" sale of €1,000 to themselves. They calculate the VAT (e.g., 20% or €200). They pay this €200 to their government (Output VAT) but simultaneously claim it back (Input VAT).

The Result: The net cash impact is zero, but the transaction is fully reported and compliant.

The Catch: You must prove your customer is a business. You do this by validating their VAT number. If you invoice a customer without a valid VAT number using the reverse charge, auditors will assume the customer is a consumer. You will then be held liable for the VAT you failed to collect, plus interest and penalties.

Digital Services and the One Stop Shop (OSS)

For US businesses selling digital products to consumers (B2C) in the EU, the compliance burden is significant. Since you must charge VAT at the rate of the consumer's country (27 different rates), you technically need to register in every country.

To simplify this, the EU introduced the One Stop Shop (OSS).

Non-Union OSS: This scheme allows non-EU businesses (like those in the US) to register for VAT in just one EU member state (e.g., Ireland or the Netherlands).

Simplified Reporting: You collect VAT from all your EU customers at their respective rates. You then file a single quarterly return to your host country, remitting the total tax collected. The host country distributes the funds to the other member states.

No Thresholds: Be aware that the "de minimis" threshold (which allowed small shipments to be tax-free) has been abolished. Virtually all digital sales into the EU are taxable from the first cent.

Financial Mechanics and FX Risk

Getting the invoice right is only half the battle. The other half is ensuring that the money you receive retains its value. Cross-border payments are subject to hidden fees, exchange rate volatility, and settlement delays that can erode profit margins by 3-5% or more.

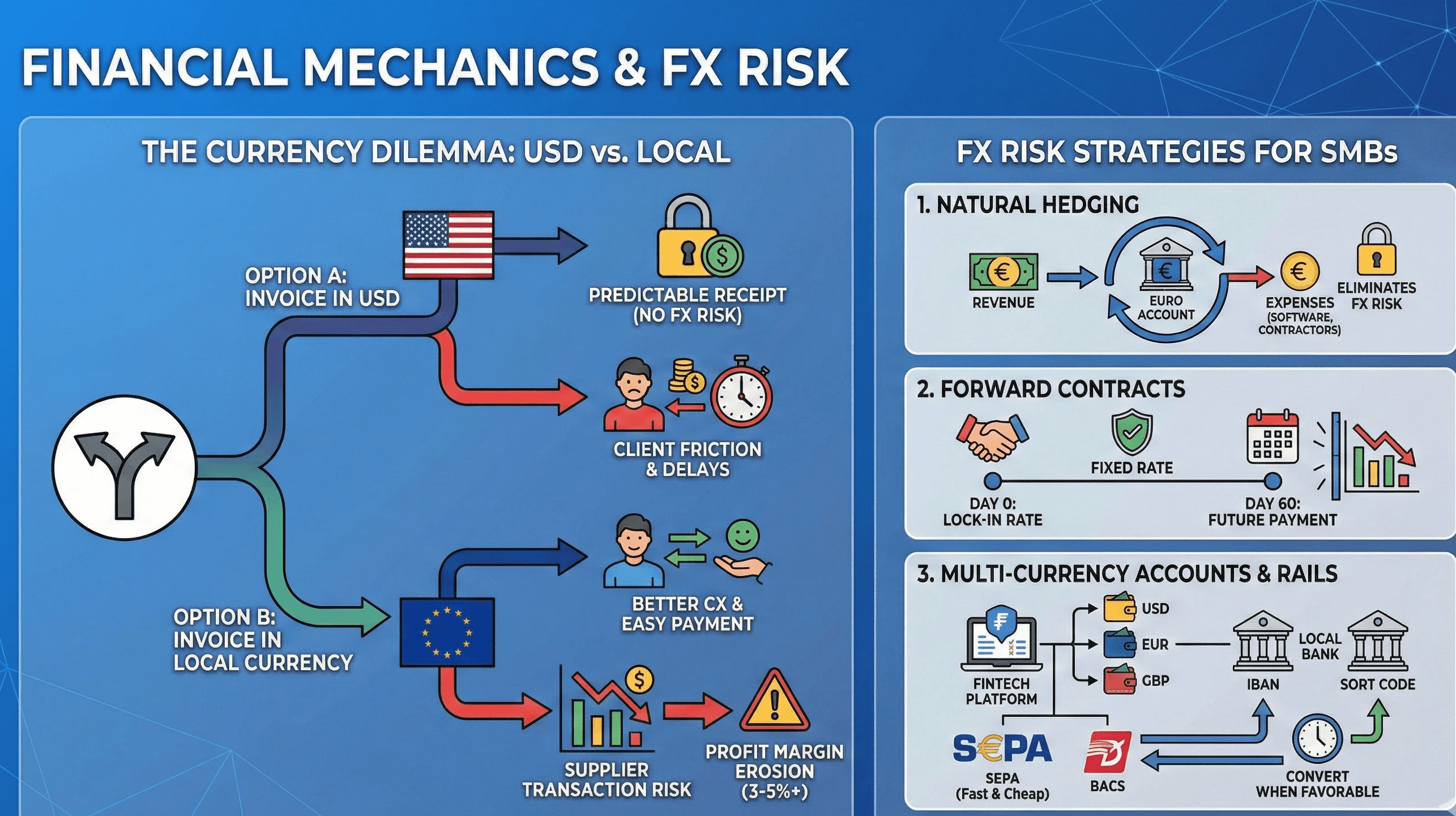

The Currency Dilemma: USD vs. Local Currency

When sending an invoice, you face a strategic choice: invoice in your own currency (USD) or your client's currency (e.g., EUR, GBP, CAD)?

Option A: Invoicing in USD

Pros: You know exactly how much you will receive. The risk of currency fluctuation is pushed entirely to the client.

Cons: It creates friction. The client may have to pay high FX fees to their bank to send USD. They may delay payment while waiting for a favorable exchange rate. It can be a competitive disadvantage compared to vendors who bill in local currency.

Option B: Invoicing in Local Currency (e.g., EUR)

Pros: Better Customer Experience (CX). The client pays exactly what they see on the invoice, often via a cheaper local transfer. It signals commitment to the market.

Cons: You bear the Transaction Risk. If the Euro weakens against the Dollar between the day you send the invoice and the day you get paid, your revenue in USD terms drops.

Strategies for Managing FX Risk

For SMBs who cannot access complex hedging instruments, there are practical ways to manage this risk:

Natural Hedging: If you have expenses in the same currency as your revenue, you can create a natural hedge. For example, if you earn revenue in Euros from clients and pay for European software or contractors in Euros, keep the funds in a Euro account. Never convert them back to USD. This eliminates FX risk entirely for that portion of cash flow.

Forward Contracts: If you have a large, predictable inflow (e.g., a $100,000 payment due in 60 days), you can use a forward contract with a currency broker. This allows you to "lock in" today's exchange rate for that future date. You lose the upside if the rate improves, but you are protected against the downside.

Multi-Currency Accounts: Fintech platforms like Wise, Revolut, or Airwallex offer multi-currency business accounts. These provide you with local bank details (e.g., a European IBAN, a UK Sort Code). Clients can pay you via their local banking rails (SEPA in Europe, BACS in the UK), which is often free and instant. You then hold the funds in that currency and convert them only when the rate is favorable.

The Payment Rails: Speed vs. Cost

SWIFT: The traditional network for international wires. It is reliable but slow (1-5 days) and expensive. "Intermediary banks" often deduct fees ($20-$50) along the way, meaning the amount you receive is less than the amount invoiced, causing reconciliation headaches.

SEPA (Single Euro Payments Area): The standard for Euro payments. It is incredibly fast and cheap (often cents). US businesses can access SEPA via virtual IBANs.

Credit Cards: The fastest option for settlement. However, merchant fees (approx. 3%) and potential cross-border surcharges can eat into margins. It is often best reserved for lower-value, high-volume transactions.

The High Cost of Non-Compliance

Ignoring these complexities is not an option. The cost of non-compliance goes beyond potential fines; it directly impacts operational efficiency and cash flow.

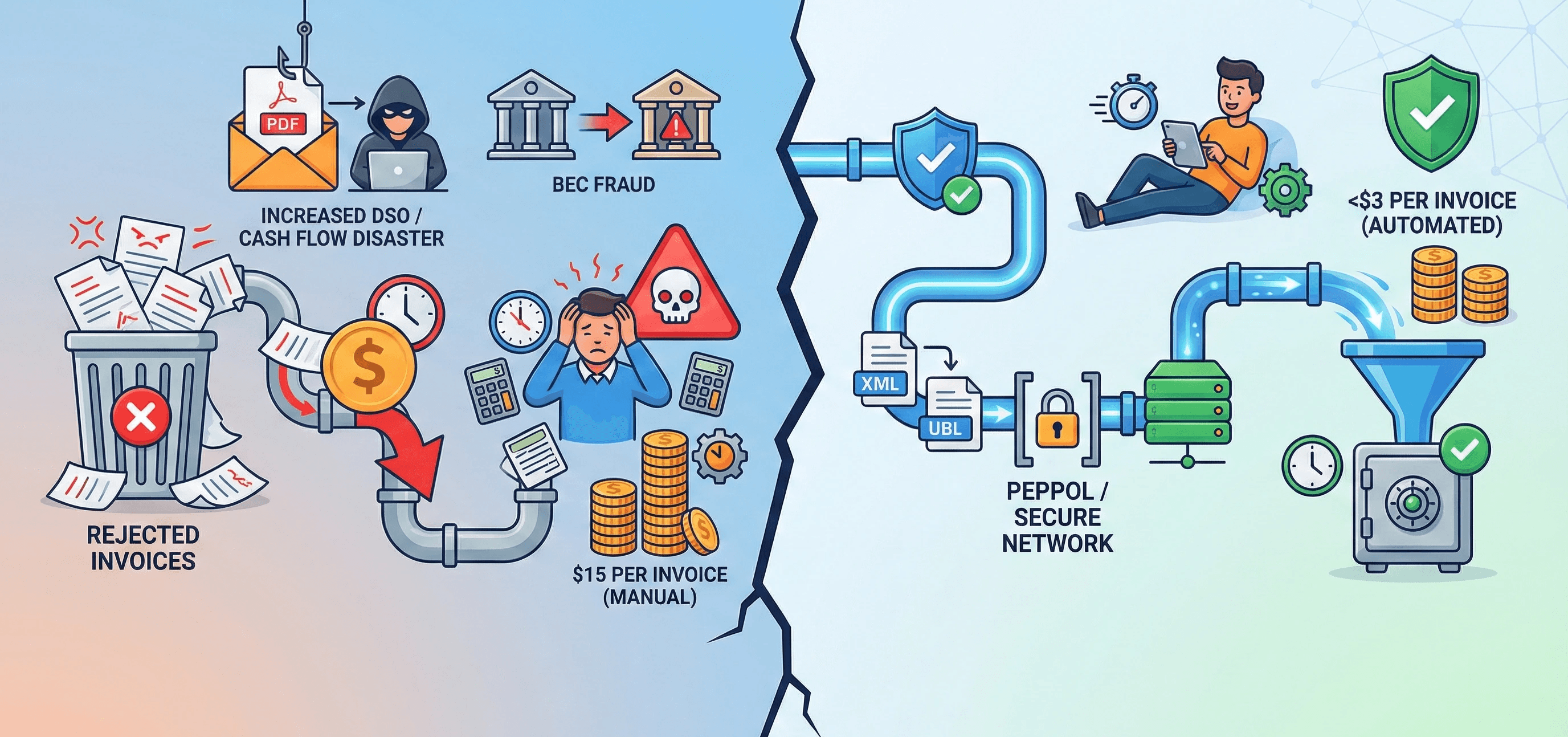

The Surge in Invoice Rejections

In the early months of 2025, global invoice rejections surged by 273%. This was not due to a sudden decline in client solvency, but rather the tightening of automated AP systems. As businesses adopt stricter compliance rules to meet government mandates, their systems are rejecting any invoice that fails validation checks (e.g., invalid PO number, missing tax code, wrong address format).

A rejected invoice is a cash flow disaster. It requires manual intervention to investigate the error, correct the document, and resubmit it. This process can add weeks to the collection cycle, significantly increasing Days Sales Outstanding (DSO).

The Fraud Vector: Business Email Compromise (BEC)

Manual invoicing processes, specifically sending PDF invoices via email, are highly vulnerable to Business Email Compromise (BEC). Fraudsters infiltrate email servers, intercept legitimate invoices, and alter the banking details before the client receives them.

Statistic: 79% of corporate practitioners reported experiencing payment fraud attempts in 2024.

The Solution: Moving to secure, structured networks like Peppol drastically reduces this risk. In the 4-corner model, the sender's identity is authenticated by their Access Point, ensuring that the invoice (and the bank details within it) genuinely originated from the supplier.

Operational Drag

The hidden cost of manual international invoicing is the time your team spends managing it. Manually looking up VAT rates, verifying tax IDs, calculating exchange rates, and chasing clients across time zones is a massive drain on productivity. Studies show that manual processing costs can be up to $15 per invoice, compared to less than $3 for automated processing.

Automation – The Strategic Imperative

Given the complexity of country-specific mandates, the financial risks of currency fluctuation, and the operational burden of manual processing, automation is no longer a "nice to have", it is a strategic imperative.

The Role of Modern ERPs

Modern Enterprise Resource Planning (ERP) systems like NetSuite, Microsoft Dynamics, and SAP are evolving to handle these complexities. They are integrating "Electronic Invoicing" modules that connect directly to government portals or Peppol access points.

NetSuite: Offers capabilities to generate e-documents (XML/JSON) and integrates with tax engines to automate rate determination based on the complex "Place of Supply" rules.

QuickBooks Online: For smaller businesses, QBO can handle international invoicing but often requires the use of "Custom Fields" to capture mandatory data like VAT numbers, and may need third-party apps to handle complex e-invoicing formats.

AI-Driven Collections: The Abivo Advantage

This is where specialized automation platforms like Abivo provide a critical advantage. While ERPs handle the generation of the invoice, Abivo handles the lifecycle of the payment.

For businesses generating over 500 invoices a month, manual follow-up is mathematically impossible to scale effectively. Abivo utilizes AI-powered agents (like "Kate") to bridge the gap.

Automated Dispute Resolution: One of the biggest causes of late international payments is unresolved disputes—often over minor administrative errors like a missing PO number. Abivo's AI agents can engage with the client's AP department, identify the discrepancy, and trigger the necessary internal workflows to correct and resubmit the invoice without human intervention.

Predictive Compliance: By analyzing historical data, AI can predict which invoices are likely to be rejected based on the client's past behavior or specific portal requirements. This allows your team to fix errors before the invoice is sent, preventing the rejection cycle entirely.

24/7 Global Coverage: Your AR team sleeps; your global clients do not. Abivo’s AI agents operate around the clock, chasing payments and resolving queries in the client's time zone. This eliminates the "email tag" delays caused by time differences.

Seamless Integration: Abivo integrates with the platforms you already use, QuickBooks, NetSuite, Xero, Stripe, and more, adding a layer of intelligence on top of your existing financial stack.

Strategic Playbook for Finance Leaders

To transform your international collections from a liability into a strength, implement this strategic playbook.

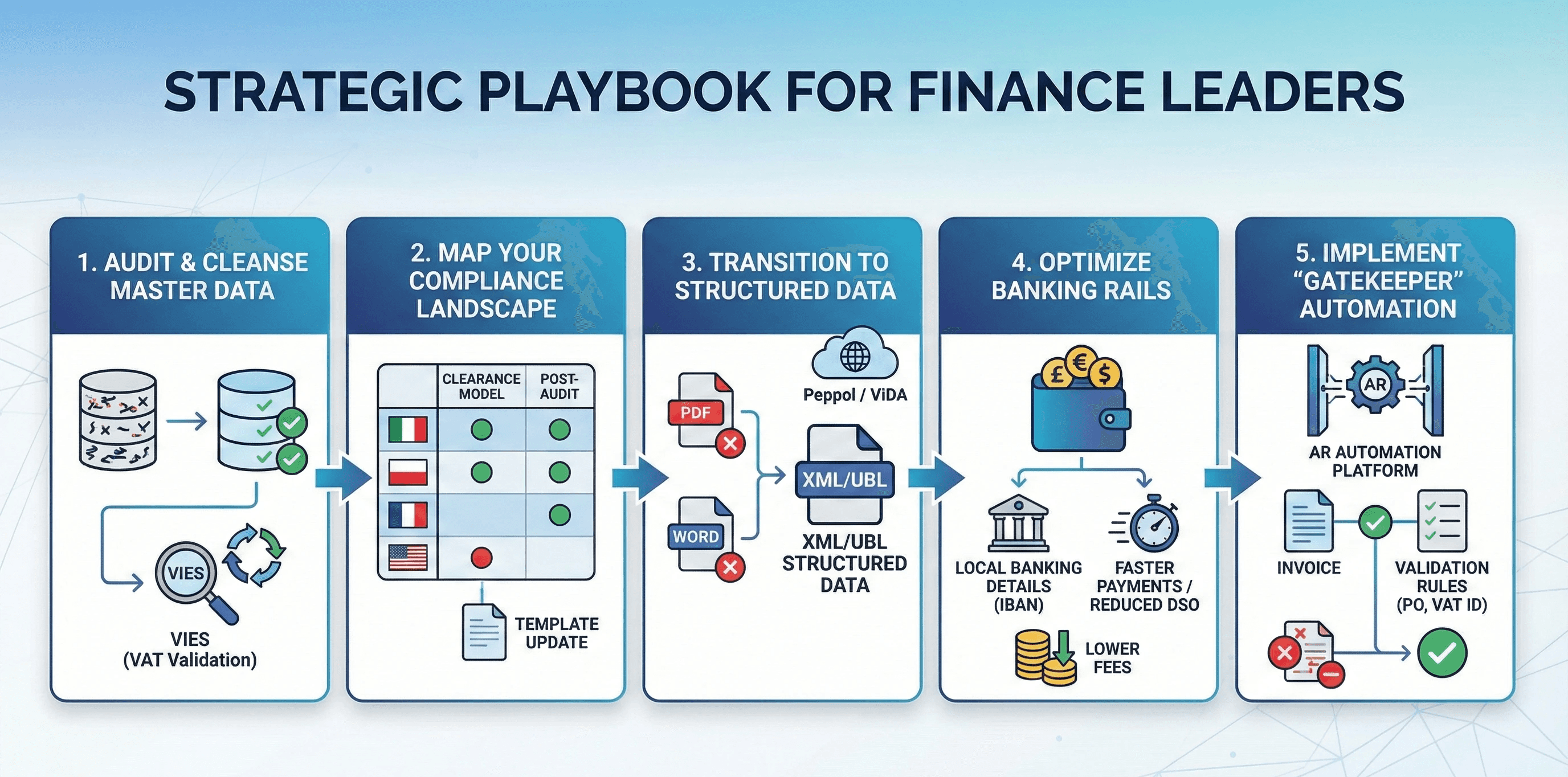

1. Audit and Cleanse Master Data

The most common cause of invoice rejection is bad data.

Action: Run a comprehensive audit of your customer master data. Ensure every international client record includes a valid, active VAT/Tax ID.

Tool: Use the EU's VIES (VAT Information Exchange System) tool to batch-validate European VAT numbers. Automate this check to run quarterly, as tax statuses can change.

2. Map Your Compliance Landscape

Don't guess; know the rules for your markets.

Action: Create a "Compliance Matrix" for your top 5 export destinations. Identify which countries use a Clearance Model (like Italy, Poland) and which use a Post-Audit model.

Template Update: Adjust your invoice templates in your ERP to ensure they support the specific mandatory fields (e.g., Fiscal Rep, HS Codes) required for those high-priority markets.

3. Transition to Structured Data

Stop relying on PDF and Word documents as your primary invoice format.

Action: Begin the transition to structured data (XML/UBL). Even if your current clients don't mandate it yet, the global trend toward Peppol and ViDA makes this inevitable. Adopting a platform that supports e-invoicing now will future-proof your operations.

4. Optimize Banking Rails

Stop losing 3-5% of your revenue to banking friction.

Action: Open multi-currency accounts (via providers like Wise or Airwallex) to gather local banking details (IBANs, Sort Codes).

Policy: Update your invoices to display these local bank details for your international clients. This makes it cheaper and faster for them to pay you, reducing DSO.

5. Implement "Gatekeeper" Automation

Prevent errors before they leave your system.

Action: Deploy AR automation tools that validate invoice data against configured rules before transmission. Ensure that no invoice can be sent if a mandatory field (like a PO number or VAT ID) is missing.

Conclusion

The era of the static, paper-based invoice is ending. We are entering a new paradigm where an invoice is a dynamic, digital data packet that must navigate a complex ecosystem of tax portals, banking networks, and compliance filters before it can result in payment.

For businesses invoicing overseas, this presents a clear choice. You can cling to manual processes, accepting the high costs of rejection, fraud risk, and delayed cash flow. Or, you can embrace the shift. By understanding the regulatory landscape, from the strictures of ViDA to the mechanics of the Reverse Charge, and leveraging technologies like AI-driven automation from Abivo, you can turn global collections into a streamlined, predictable, and profitable operation.

The goal is not just to get paid. It is to build a financial operation that is robust enough to withstand the scrutiny of tax authorities and agile enough to support your business's global ambitions. The tools and knowledge are available; the time to act is now.