The Liquidity Bridge: A Definitive Guide to Managing Accounts Receivable in Mergers & Acquisitions

Discover critical AR considerations for M&A success including due diligence insights, Day One readiness, system integration strategies, and automation benefits that protect cash flow during transitions.

Sia Ghazvinian

Co-Founder & CEO

Table of contents

Share

The Silent Value Destroyer in Deal-Making

The landscape of modern Mergers and Acquisitions (M&A) is littered with the wreckage of transactions that looked pristine on a spreadsheet but failed in the crucible of operational reality. While dealmakers often fixate on revenue synergies, market share expansion, and intellectual property acquisition, the silent engine of the acquired business, its working capital cycle, is frequently left to sputter. Accounts Receivable (A/R), the most liquid and sensitive component of this cycle, represents the intersection of financial health and customer trust. It is here, in the mundane details of invoicing, collections, and cash application, that the theoretical value of a merger is either secured or squandered.

Recent market analysis indicates a sobering statistic: between 70% and 90% of M&A transactions fail to achieve their projected value.1 While the causes are multifactorial, ranging from cultural misalignment to macro-economic shifts, a significant portion of this "value leakage" occurs in the first 100 days post-close, specifically within the Order-to-Cash (O2C) cycle. When two entities merge, the friction generated by combining disparate billing systems, conflicting credit policies, and overlapping customer bases can cause Days Sales Outstanding (DSO) to spike, creating a liquidity crunch exactly when cash is most needed to fund integration costs.

This report serves as an exhaustive operational and strategic manual for financial leaders tasked with the stewardship of Accounts Receivable during corporate transitions. It moves beyond the high-level platitudes of "synergy" to examine the granular mechanics of the transition. We will explore the rigorous demands of pre-deal due diligence, where the quality of the receivables asset is verified against the risk of "ghost assets" and "channel stuffing." We will dissect the legal and structural frameworks required to transfer the rights to payment, navigating the complex web of anti-trust regulations and banking covenants. We will delve into the technical abyss of ERP migration, providing a roadmap for moving data from legacy systems like QuickBooks to enterprise-grade platforms like NetSuite without losing transaction fidelity. Finally, we will illuminate the emerging role of Artificial Intelligence, specifically Agentic AI and Large Language Models (LLMs), in reconciling the chaotic data streams that characterize the post-merger environment.

The central thesis of this analysis is that AR integration is not merely a back-office accounting task; it is a strategic imperative that serves as the first line of defense against revenue leakage and customer attrition. By treating the O2C cycle as a distinct workstream with its own governance, technology stack, and cultural roadmap, acquirers can ensure that the bridge between deal signing and value realization remains unbroken.

The Anatomy of the Asset: Valuation and Pre-Deal Due Diligence

Before a single line of code is migrated or a single customer is notified, the acquiring entity must establish a microscopic understanding of what they are actually buying. In the context of M&A, the Accounts Receivable sub-ledger is not just a list of debts; it is a forensic artifact that reveals the target company's operational discipline, the health of its customer relationships, and the veracity of its reported revenue.

Quality of Earnings (QoE) and the Integrity of Receivables

The Quality of Earnings (QoE) report is the bedrock of valuation, and the receivables analysis within it is designed to strip away accounting artifices to reveal the true cash-generating capability of the business. The acquirer’s diligence team must look past the net realizable value presented on the balance sheet and interrogate the underlying "collectibility" of the portfolio.

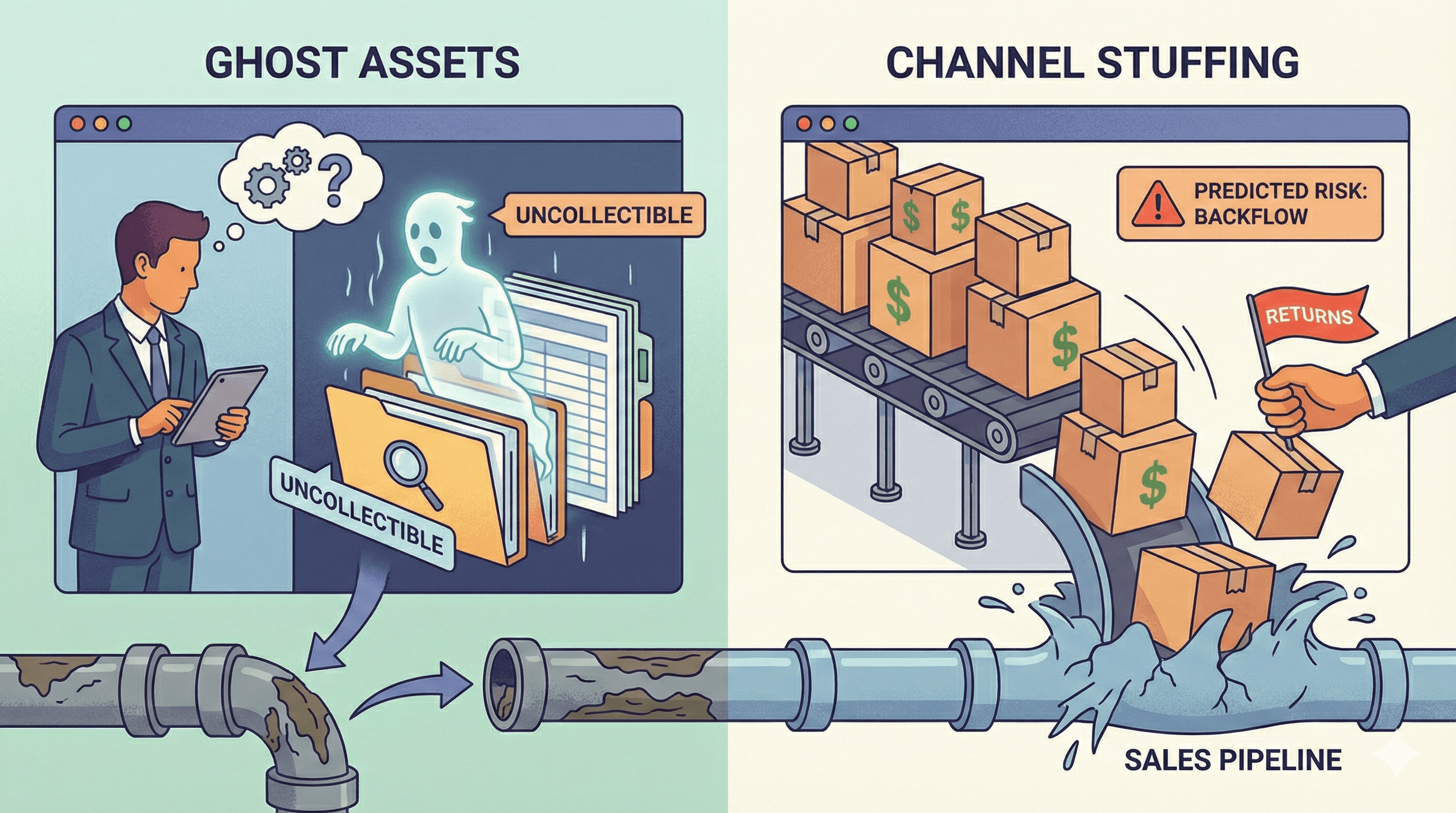

The Phenomenon of "Ghost Assets" in Receivables

A pervasive risk in lower-middle-market transactions is the presence of "ghost assets" within the receivables ledger. While the term is traditionally applied to fixed assets, machinery or equipment that appears on the register but has been lost, stolen, or scrapped, it has a parallel in working capital. In the AR context, a ghost asset is a receivable that remains on the aging report despite being uncollectible.

These phantom balances often accumulate due to:

Operational Neglect: Small residual balances (e.g., $0.50 short-payments) that were never written off because the manual effort required exceeded the value, yet in aggregate, across thousands of transactions, they distort the ledger.

Dispute Stagnation: Invoices that have been disputed by customers for valid reasons (e.g., damaged goods, pricing errors) but remain "open" because the target company lacks a robust dispute resolution workflow or credit note approval hierarchy.

Intentional Inflation: In more nefarious scenarios, management may intentionally avoid writing off bad debt to preserve EBITDA figures leading up to a sale process. This artificially inflates the asset base and suppresses the bad debt expense line item.

To identify these ghosts, diligence teams must perform a "Roll-Rate Analysis." Unlike a static aging report which shows the status at a single point in time, a roll-rate analysis tracks cohorts of invoices over time to see the probability of a receivable moving from "Current" to "30 Days Past Due," then to "60 Days," and so on. A deterioration in these transition rates, specifically a "bulge" in the 90+ day bucket that does not resolve, is a primary indicator of low-quality receivables that must be excluded from the purchase price or heavily reserved against.

The "Channel Stuffing" Red Flag

Another critical aspect of AR diligence is detecting "channel stuffing." This practice involves accelerating sales into the current period, often by offering extended payment terms or unofficial rights of return, to meet revenue targets before a transaction.

Symptoms of Channel Stuffing in AR Data:

Spike in Quarter-End Billings: A disproportionate volume of invoices generated in the final three days of the reporting period.

Abnormal DSO Spikes: If revenue is rising but cash collections are flat or declining, the "quality" of that revenue is suspect.

Extended Terms: A sudden shift in the customer master data showing terms moving from Net 30 to Net 90 for key accounts without a corresponding commercial rationale.

If diligence reveals channel stuffing, the acquirer faces a "double dip" loss post-close: first, the cash flow is delayed due to the extended terms; second, there is a high risk of product returns or credit requests in the post-close period, effectively reversing the revenue that was paid for in the acquisition multiple.

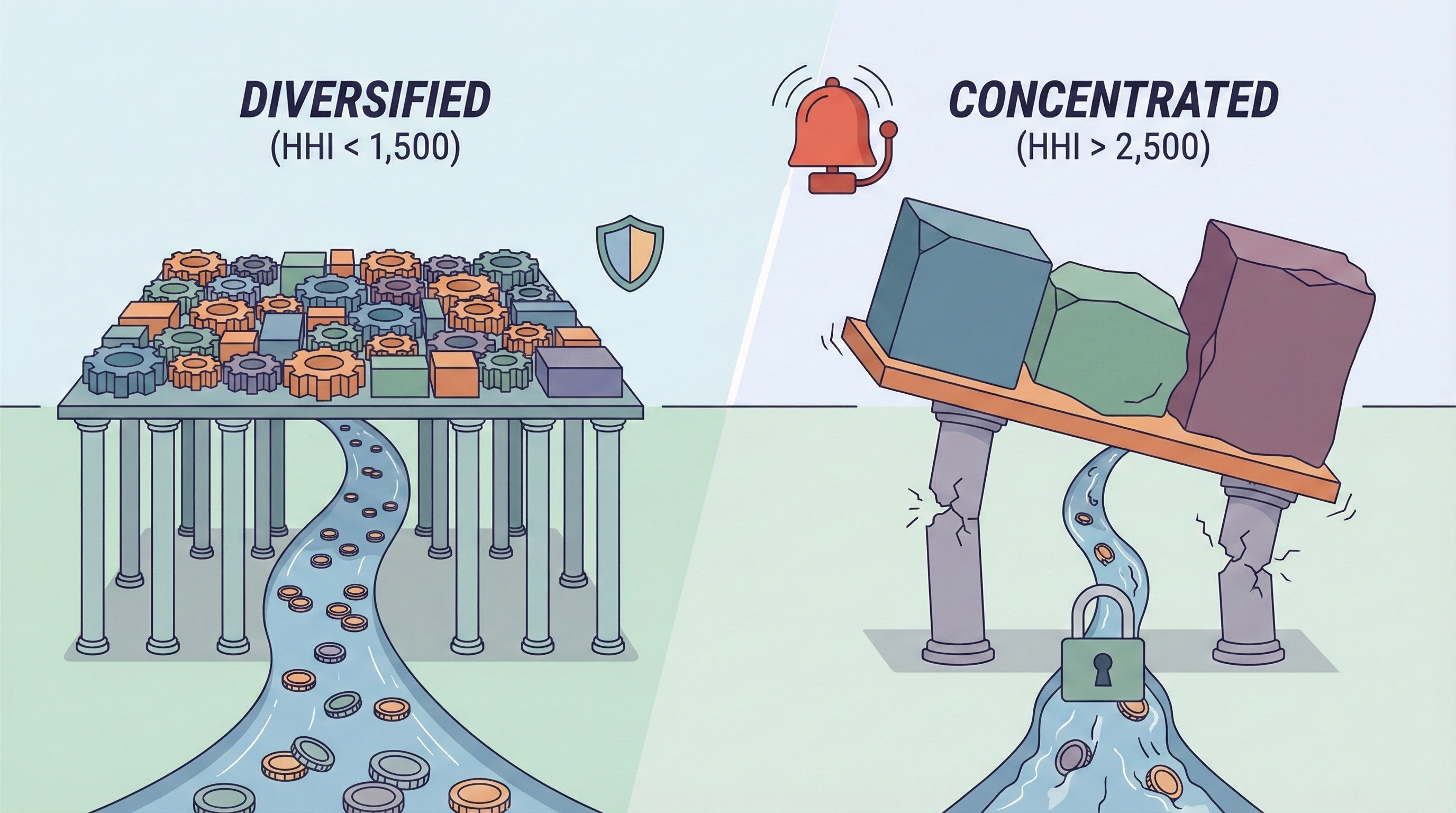

Concentration Risk and the Herfindahl-Hirschman Index

Accounts receivable concentration is a significant valuation variable. If a target company relies on a small cluster of customers for the majority of its cash flow, the risk profile of the asset changes dramatically. The departure of a single key client post-merger, perhaps due to dissatisfaction with the new ownership or a change in strategic direction, can render a significant portion of the AR valuation worthless.

To quantify this, sophisticated diligence teams utilize the Herfindahl-Hirschman Index (HHI). While typically used to measure market competition, in this context, it measures the concentration of the receivables portfolio. A high HHI score indicates that the liquidity of the target is held hostage by a few dominant payers.

Strategic Implications of AR Concentration Levels

Concentration Level | HHI Score Indicator | Operational Risk Profile | M&A Mitigation Strategy |

Highly Diversified | Low (< 1,500) | Low Risk. Loss of any single account is immaterial to working capital. | Standard integration. Collections can be automated/centralized immediately. |

Moderate Concentration | Medium (1,500 - 2,500) | Medium Risk. Top 10 customers dictate cash flow cadence. | "White Glove" transition required for top accounts. Personal outreach by leadership. |

High Concentration | High (> 2,500) | Critical Risk. The target is effectively a subcontractor to a few major firms. | Integration is contingent on customer retention. "Key Man" clauses may be needed for sales staff owning these relationships. |

The Working Capital "Peg" and the Negotiation of "Current" Assets

The transition from valuation to contract negotiation centers on the "Working Capital Peg." In most M&A Purchase Agreements, the buyer and seller agree on a "target" level of working capital (Current Assets minus Current Liabilities) that must be delivered at closing. This target, or "Peg," is usually the average working capital over the trailing 12 months.

If the actual working capital at closing is higher than the Peg, the buyer pays the seller the difference. If it is lower, the purchase price is reduced. This mechanism protects the buyer from the seller "draining the tank", collecting all receivables aggressively while delaying payables, prior to handing over the keys.

The Negotiation Battleground:

The definition of "Current Assets" is fiercely debated. Buyers will argue to exclude "aged" receivables (e.g., >90 days) from the calculation of actual working capital. Their argument is that these assets are effectively bad debt and should not count toward the Peg. Sellers will argue that these are valid, collectible amounts and should be included.

The Buyer's Strategy: Demand a strict definition of "Net Working Capital" that excludes any receivable older than 90 days, any receivable from a customer currently in bankruptcy, and any portion of a receivable subject to a dispute. This lowers the "Actual" working capital number, potentially triggering a purchase price reduction in the buyer's favor.

The Seller's Strategy: Perform a "specific identification" of aged items to prove collectibility (e.g., "Customer X always pays in 100 days, here is the history"). They will argue for a "normalization" adjustment to the Peg to account for seasonality or one-off events.

Days Sales Outstanding (DSO) as a Proxy for Operational Efficiency

Days Sales Outstanding (DSO) is the standard metric for measuring the speed of the O2C cycle. In M&A, analyzing the target's DSO against industry benchmarks offers crucial insights into both risk and opportunity.

Benchmarking for Synergy:

If the acquirer operates with a DSO of 35 days and acquires a competitor operating at 55 days, this delta represents a "Working Capital Synergy." By applying the acquirer’s more rigorous credit policies and collections technologies to the target’s portfolio, the combined entity can release significant cash from the balance sheet.

However, realizing this synergy is fraught with danger. A sudden tightening of credit terms (e.g., forcing a customer from Net 60 to Net 30) can be perceived as a hostile act by the customer base. Integration teams must model the "elasticity" of the customer base, how sensitive are they to term changes? For industries where terms are dictated by the buyer (e.g., retail giants like Walmart), the acquirer may have zero leverage to improve DSO, regardless of their internal efficiency.

DSO Variance Analysis in M&A Scenarios

DSO Scenario | Operational Diagnosis | Integration Implication |

Target DSO << Industry Average | Highly efficient or overly restrictive credit policy stifling sales. | Caution: Relaxing terms might spur growth but requires funding. Integration should focus on maintaining this efficiency. |

Target DSO >> Industry Average | Lax collections, poor dispute resolution, or "banking" the customer. | Opportunity: Prime candidate for "Working Capital Release." Implement acquirer's automated collections tools immediately. |

Volatile DSO (Sawtooth Pattern) | Seasonal sales spikes or "quarter-end" sales pushing. | Risk: Cash flow forecasting will be difficult. Requires a flexible liquidity buffer post-close. |

The Architecture of Integration: Legal, Structural, and Clean Room Protocols

Before the operational teams can begin the work of combining ledgers, a rigorous legal and structural framework must be established. This phase determines the "rules of engagement" for how data is shared, how money moves, and how the legal rights to payment are transferred.

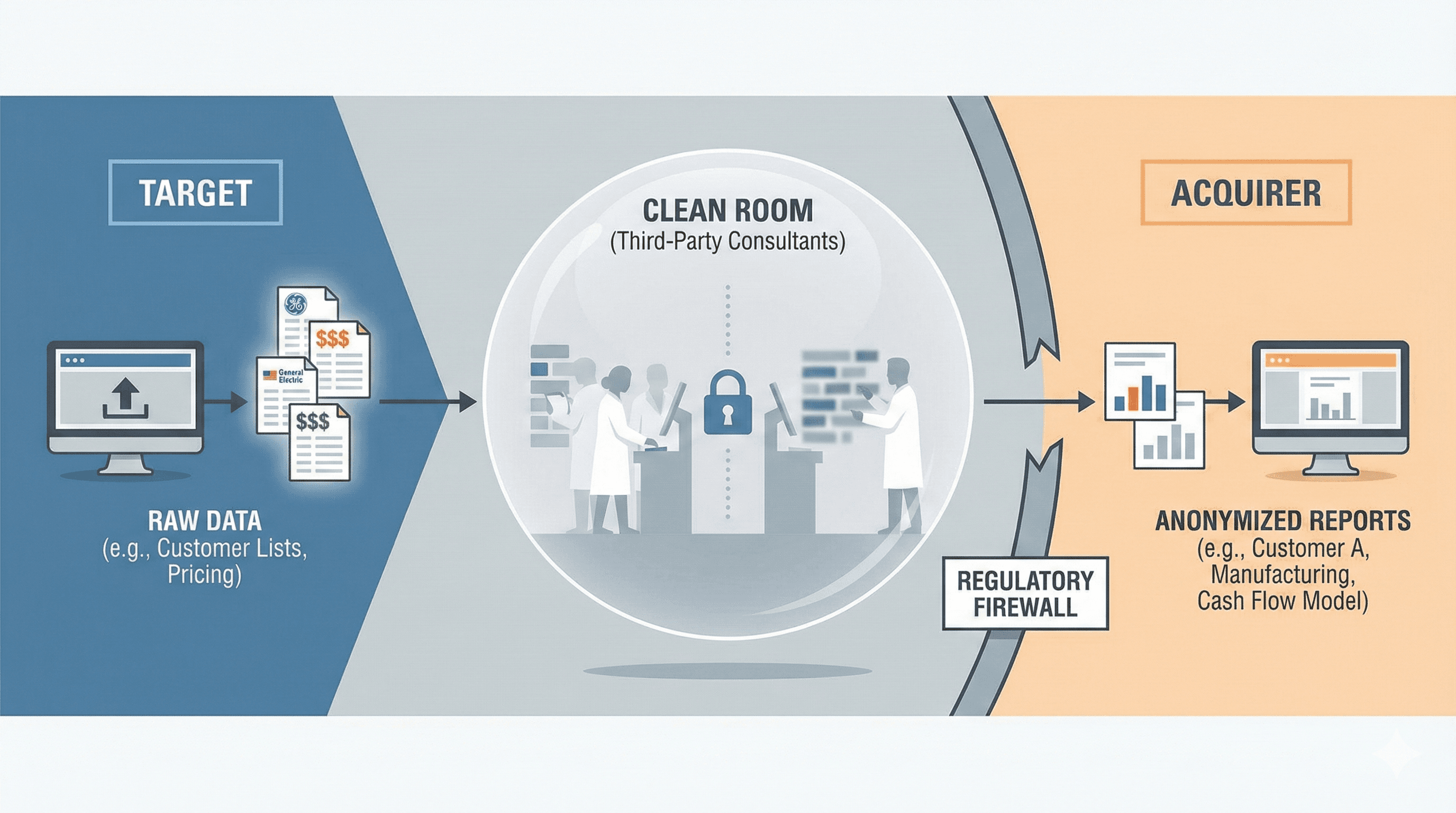

The "Clean Room": Navigating Anti-Trust in Data Analysis

In transactions involving competitors, anti-trust laws (such as the Hart-Scott-Rodino Act in the U.S.) strictly prohibit the sharing of competitively sensitive information prior to regulatory approval.8 Customer lists, specific pricing terms, and granular aging reports fall squarely into this category. If the deal were to collapse, the target would be harmed if the acquirer knew exactly which customers were late payers or what specific prices they were paying.

To navigate this, companies utilize a "Clean Room" environment.

Definition: A Clean Room is a secure, isolated data environment managed by third-party consultants (e.g., Corcentric, Deloitte, KPMG).

Mechanism: The target company uploads raw, unredacted AR files into the Clean Room. The consultants analyze the data and provide aggregated reports to the acquirer’s integration team.

The Output: Instead of seeing "General Electric owes $5M and pays in 65 days," the acquirer sees "Customer A (Industry: Manufacturing) owes $5M and pays in 65 days."

The Goal: This allows the acquirer to model cash flows, assess credit risk, and plan for potential customer overlaps without violating "gun-jumping" regulations. Only after the deal formally closes (or receives anti-trust clearance) can the blinders be removed.

Legal Assignment of Receivables

The transfer of the right to collect a debt is a legal process known as "Assignment." The structure of the deal, Asset Purchase vs. Stock Purchase, dictates the complexity of this process.

Stock Purchase: The acquirer buys the shares of the target entity. The legal entity remains intact, meaning the contracts with customers and the ownership of the receivables do not technically change hands. This is the simplest path for AR integration as it requires minimal customer consent.

Asset Purchase: The acquirer buys specific assets of the target, including the AR ledger. This is legally complex. The acquirer must ensure that customer contracts do not contain "anti-assignment" clauses. If they do, the target must obtain "Consent to Assign" from every affected customer, a logistical nightmare that can delay closing.

Notice of Assignment: regardless of the deal structure, customers must eventually be notified to direct payments to the new owner. Under the Uniform Commercial Code (UCC) in the U.S., a debtor (customer) is discharged from their obligation if they pay the assignor (seller) until they receive notification that the right to payment has been assigned to the assignee (buyer). Therefore, the "Notice of Assignment" letter is not just a courtesy; it is a legal necessity to enforce payment.

Transition Service Agreements (TSA) and the Billing Bridge

It is rare for an acquirer to be ready to migrate the target’s billing operations on Day 1. To bridge the gap, the parties execute a Transition Service Agreement (TSA).

Under a TSA, the seller agrees to continue performing back-office functions, such as generating invoices, applying cash, and managing disputes, on behalf of the buyer for a specified period (typically 3 to 12 months).

The Strategic Risk: While TSAs ensure continuity, they can become a crutch. If the TSA is priced attractively (e.g., at cost), the acquirer may lack the urgency to migrate systems. Conversely, if the TSA is expensive, it drains the synergy value.

Service Level Agreements (SLAs): The TSA must include strict SLAs for AR performance. For example, "Invoices must be generated within 24 hours of shipment," or "Cash must be applied within 48 hours of receipt." Without these, the seller (who is exiting the business) has little incentive to maintain high operational standards, leading to a degradation in working capital that the buyer ultimately inherits.

Operational Integration: The First 100 Days

The "First 100 Days" is the standard cadence for M&A execution. For the Order-to-Cash function, this period is a race against entropy. The confusion inherent in a merger naturally tends toward disorder, payments getting lost, invoices going to wrong addresses, and disputes piling up. The integration strategy must actively impose order.

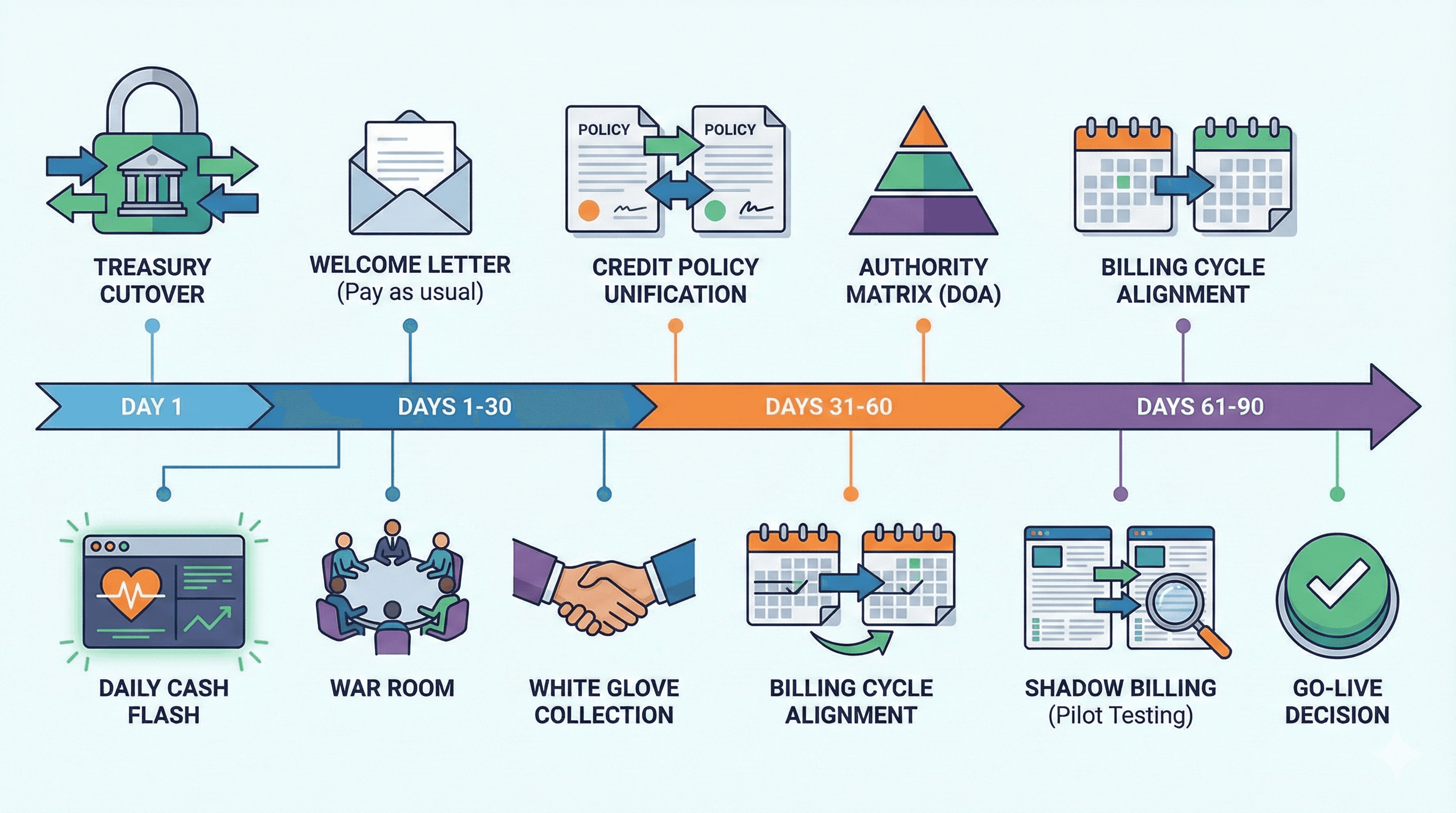

Day 1 Readiness: The "Do No Harm" Mandate

Day 1 is the day the deal closes. For AR, success on Day 1 is defined by invisibility. If a customer notices a disruption, if their portal login fails, if an invoice is late, or if a payment is rejected, the integration has stumbled out of the gate.

Key Day 1 Actions:

Treasury Cutovers: Control of the target’s bank accounts must transfer. New signatories (from the acquirer) are added; old signatories are removed.

Lockbox Sweeps: The legacy lockboxes (where customers mail checks) must remain open. A "sweep" mechanism is automated to transfer funds from these legacy accounts to the acquirer’s concentration account daily.

The "Welcome" Letter: A communication is sent to the customer base. Critically, this letter should not immediately confuse customers with complex billing changes. It should focus on the strategic value of the merger ("We are now stronger together") and reassure them of business continuity. "Please continue to pay as usual until further notice" is the safest Day 1 message.

The First 30 Days: Stabilization and Cash Visibility

Focus: Grip and Control.

During the first month, the priority is not optimization; it is visibility. The acquirer needs to know exactly how much cash is coming in daily.

Daily Cash Flash: Implement a consolidated reporting dashboard that pulls daily cash receipt totals from both the legacy and acquirer systems. This is the pulse of the integration.

The "War Room": Establish a daily stand-up meeting for the O2C team to triage issues. If a major customer’s payment fails, it is escalated and resolved in real-time.

Collection Triage: The Pareto Principle applies heavily here. The integration team should identify the top 20% of customers who represent 80% of the receivables and assign them to a "White Glove" team. Senior collectors or account managers should personally reach out to these contacts to ensure they have the correct vendor paperwork to continue paying.

Policy Freeze: Avoid making drastic changes to credit limits or payment terms in the first 30 days. The system is fragile; adding friction now will cause breakage.

Days 31-60: Policy Harmonization and Process Alignment

Focus: Alignment.

Once the immediate stabilization is achieved, the team pivots to harmonizing the rules of the road.

Credit Policy Unification: Compare the risk tolerance of both entities. Company A might require a credit application for any limit over $5,000, while Company B allows $20,000 based on history. These policies must be merged. Often, the stricter policy is adopted, which requires a communication campaign to affected customers.

Authority Matrices: Define the "Delegation of Authority" (DOA) for the combined entity. Who can approve a credit note? Who can authorize a write-off? Inconsistent DOAs are a primary source of internal fraud risk during M&A.

Billing Cycle Alignment: If Company A bills on the 1st of the month and Company B bills on the 15th, consolidating to a single billing run improves efficiency but creates a temporary cash flow gap. This "air pocket" must be forecasted and funded.

Days 61-90: The Technical Migration Pilot

Focus: Testing the Future State.

As the end of the first quarter approaches, the focus shifts to the technical migration of data (detailed in Section 5).

Shadow Billing: Run a parallel billing process where the new system generates invoices "in the background" (not sent to customers). These are compared line-by-line with the legacy system’s invoices to catch pricing errors, tax calculation differences, or missing PO numbers.

The "Go-Live" Decision: Based on the results of Shadow Billing, the leadership team makes a "Go/No-Go" decision for full system cutover.

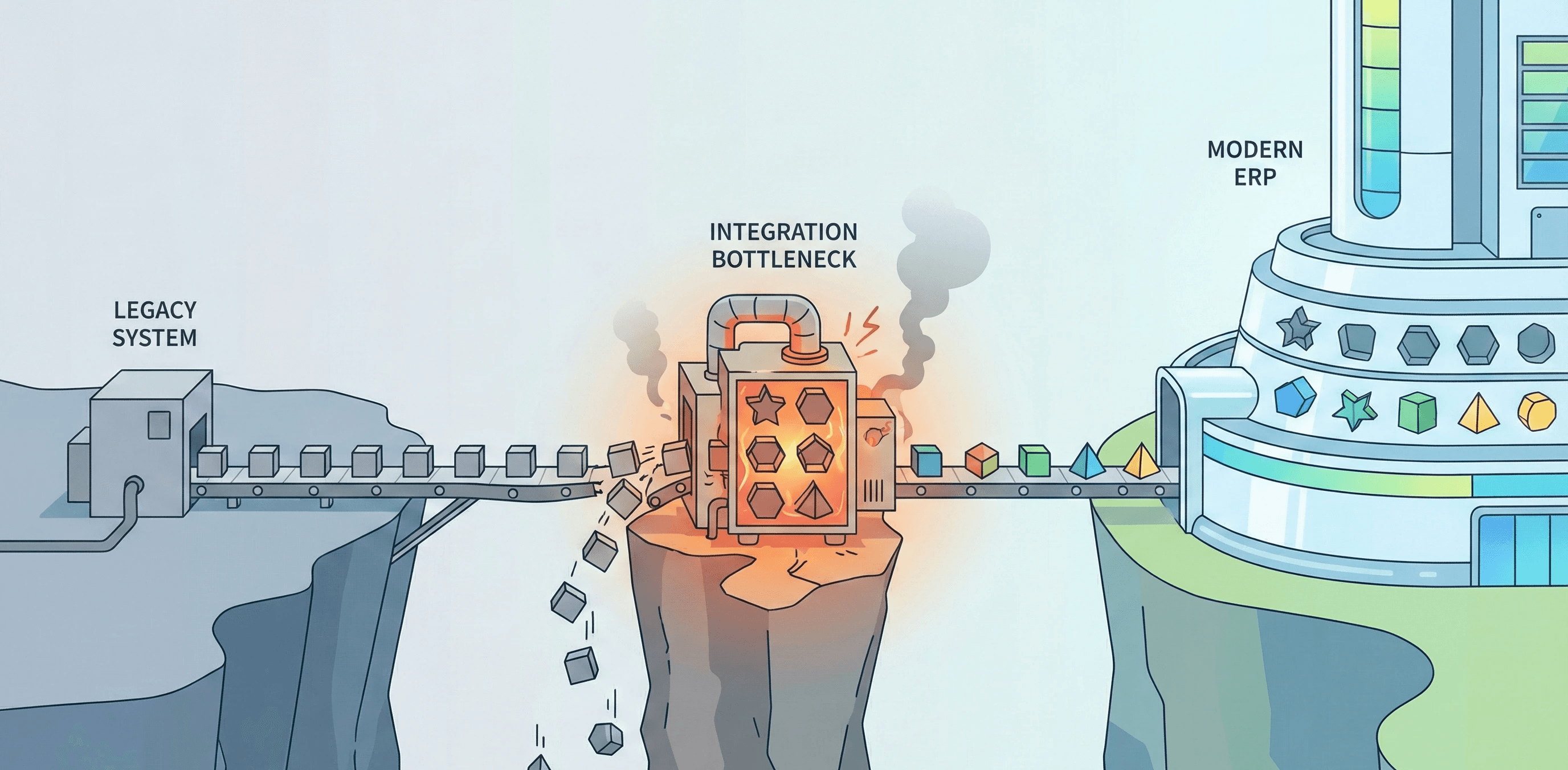

Systems Integration: The ERP Migration Challenge

The most notoriously difficult aspect of M&A integration is the consolidation of Enterprise Resource Planning (ERP) systems. In the mid-market, this often takes the form of migrating a target company from a lower-tier system (like QuickBooks, Xero, or Sage) to a Tier 1 or Tier 2 ERP (like NetSuite, SAP, or Microsoft Dynamics). This is not a simple "copy and paste" exercise; it is a translation of financial logic.

The QuickBooks to NetSuite Paradigm

This specific migration path highlights the typical challenges encountered in AR integration.

Challenge 1: Dimensionality Mismatches

QuickBooks utilizes a relatively flat data structure (Customer:Job). NetSuite, however, utilizes "Dimensional Accounting" (Subsidiary, Class, Department, Location). When exporting AR data from QuickBooks, there is often no data field that corresponds to "Department" or "Location."

The Solution: Integration teams must perform data enrichment. Before migration, every customer and invoice in the QuickBooks export must be tagged with the appropriate NetSuite dimensions. This is often a manual or semi-automated process using lookup tables in Excel or a staging database.

Challenge 2: Historical Data vs. Open Balances

A common pitfall is attempting to migrate the entire transaction history (every invoice and payment from the last 7 years). This almost always fails due to data corruption or mapping errors.

The Best Practice: The industry standard approach is to migrate only Master Data (Customer lists) and Open Balances (Unpaid invoices). Historical data is left in the legacy system, which is kept active with a single "Read-Only" license for reference/audit purposes. This strategy, often called "implanting the balance," drastically reduces risk.

Challenge 3: The Blackout Period

During the final cutover weekend, there is a "Blackout Period" where neither system is fully operational. No invoices can be raised, and no cash can be posted.

Mitigation: This period must be timed to avoid month-end or heavy billing days. The team must communicate a "cutoff" to the sales team: "Any order booked after Friday 5 PM will be held for billing until Tuesday 9 AM."

Data Cleansing and Master Data Management (MDM)

The integration is only as good as the data. Merging two customer lists inevitably results in duplication.

The Duplicate Problem: The target knows the customer as "General Electric, Inc." The acquirer knows them as "GE - Aviation Division." If these are not merged, the combined entity will have a fragmented view of credit exposure.

Fuzzy Matching: Advanced MDM tools use "fuzzy logic" algorithms to identify duplicates based on address similarity, tax IDs, or phonetic name matching.

Hierarchy Management: A critical aspect of AR integration is establishing "Parent-Child" relationships. The acquirer needs to know that "Customer A" and "Customer B" are both subsidiaries of "Global Corp" so that a single credit limit can be applied to the entire group.

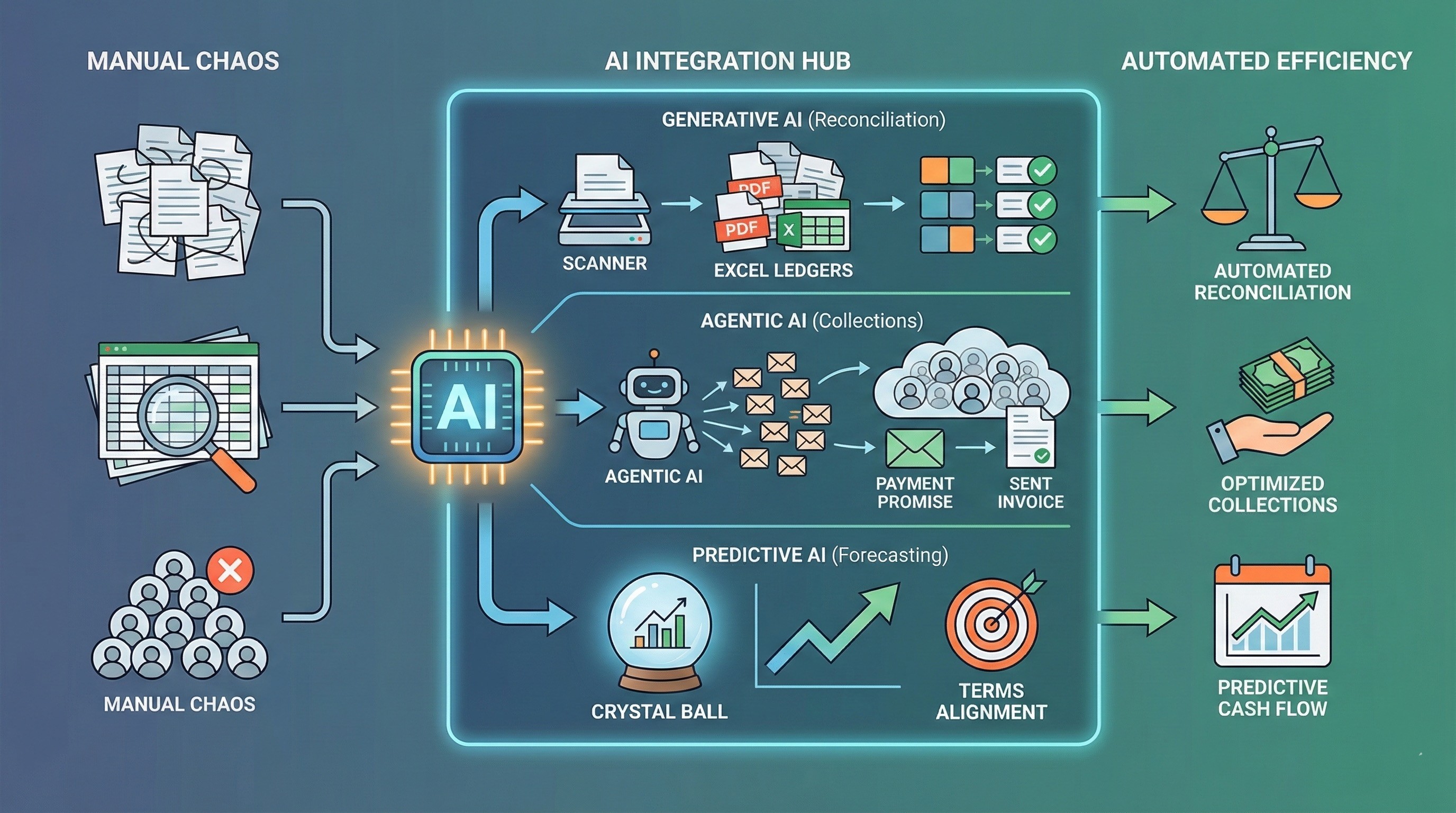

Technology and AI: The New Frontier of Integration

While traditional ERP migration is laborious, the emergence of Artificial Intelligence (AI) is providing new tools to accelerate AR integration.

Generative AI for Data Reconciliation

One of the most time-consuming tasks in post-merger accounting is reconciling the "Sub-Ledger" (the list of individual invoices) to the "General Ledger" (the total balance). Discrepancies here, caused by partial payments, unapplied cash, or currency exchange differences, can delay financial closing.

The AI Solution: Generative AI tools can ingest massive datasets, PDF bank statements, Excel sub-ledgers, and GL dumps, and identify patterns that traditional "rules-based" engines miss. For example, an AI agent can recognize that a payment of $9,985 corresponds to a $10,000 invoice minus a $15 wire fee, automatically proposing the reconciliation journal entry.

Agentic AI in Collections

"Agentic AI" refers to autonomous software agents capable of performing multi-step workflows. In the context of M&A collections, these agents are invaluable for managing the "Long Tail" of small customers.

The Use Case: During a merger, the human collections team is often overwhelmed dealing with the top 20% of accounts. This leaves the bottom 80%, thousands of smaller customers, neglected.

The Mechanism: An AI agent can autonomously email these thousands of customers, interpret their replies (using LLMs), and take action. If a customer replies, "I didn't get the invoice," the Agent retrieves the PDF from the ERP and emails it back instantly. If they say, "I will pay next week," the Agent updates the promise-to-pay date in the system. This ensures that the entire portfolio is touched, preventing leakage in the small-dollar accounts.

Predictive Cash Flow Modeling

Mergers often disrupt historical payment patterns, making cash forecasting difficult. AI models can ingest the payment history of both companies to build a predictive model for the combined entity.

Behavioral Analytics: The AI might detect that Customer X pays Company A in 30 days but takes 45 days to pay Company B. This insight allows the integration team to target Customer X for "terms alignment," pushing them to the faster payment standard.

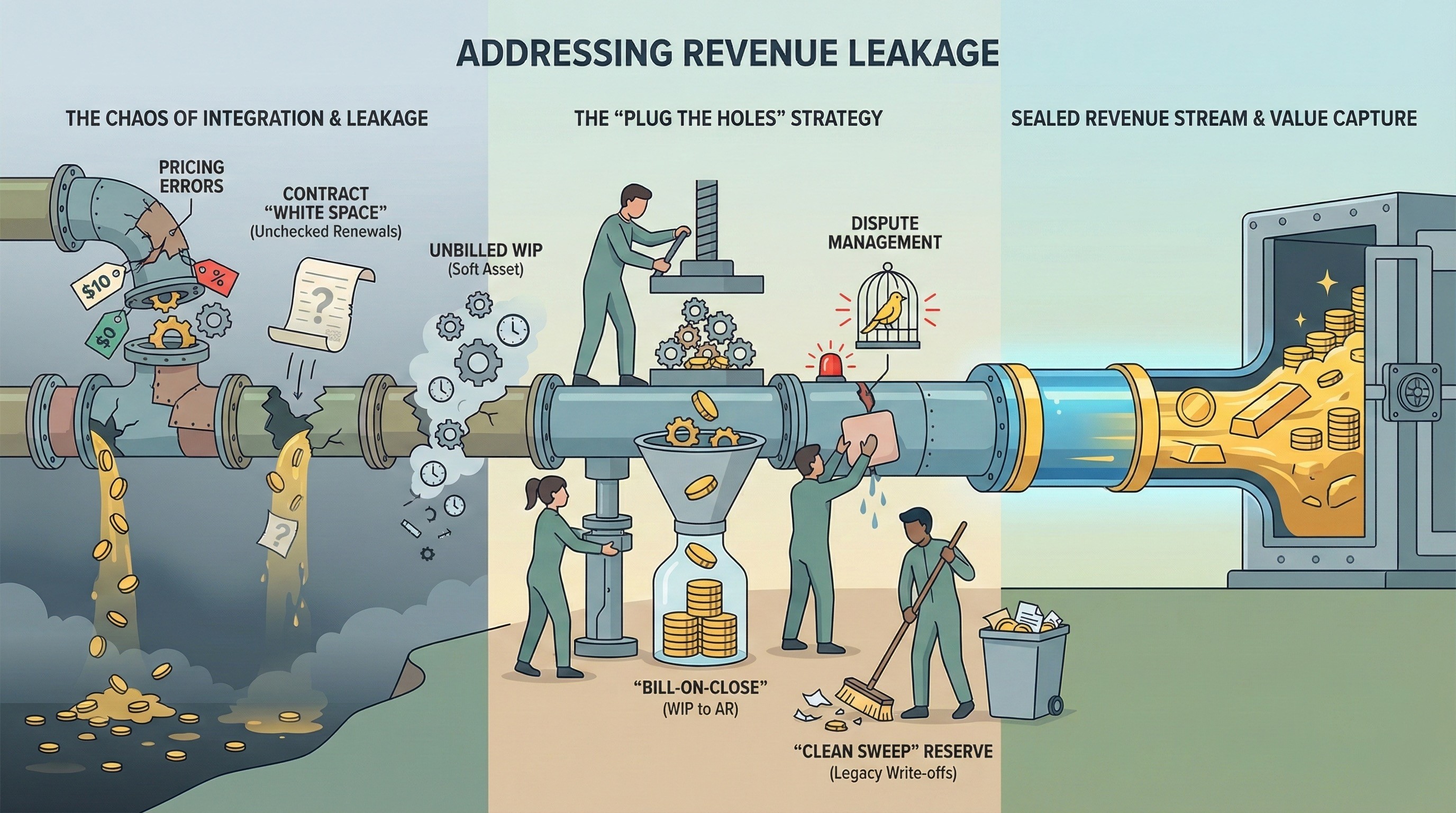

Addressing Revenue Leakage: The "Plug the Holes" Strategy

Revenue leakage is the invisible erosion of value. It occurs when a company delivers goods or services but fails to collect payment, or fails to invoice at all. In the chaos of integration, leakage creates a "death by a thousand cuts" scenario.

Sources of Integration-Induced Leakage

Pricing Errors: The most common source. The acquired company’s pricing tables (including customer-specific discounts) are not correctly migrated to the new system. The new system defaults to list price (causing disputes) or fails to apply an annual escalator (causing revenue loss).

The "White Space" in Contracts: Long-term contracts often have "white space", ambiguities regarding renewal dates or scope creep. During migration, if the "Auto-Renewal" flag is not checked in the new system, a subscription might lapse, and the service continues for free.

Unbilled Work-in-Progress (WIP): In service industries, "Work in Progress" (unbilled hours) is a volatile asset. If the cutoff procedures are not strict, hours worked in the final days of the target company’s existence may never get billed in the new system.

The "Bill-on-Close" Strategy

To mitigate WIP leakage, a robust strategy is the "Bill-on-Close" mandate.

The Protocol: The target company is instructed to run a massive billing cycle immediately prior to the closing date. The goal is to convert as much WIP and unbilled revenue as possible into Accounts Receivable.

Why: AR is a "hard" asset, it is a defined debt with a paper trail. WIP is a "soft" asset, it is an internal calculation of potential billing. It is much safer to migrate a ledger of invoices than a database of time-sheets.

Dispute Management as a Leakage Indicator

A spike in customer disputes post-merger is the "canary in the coal mine" for leakage. If disputes rise from 2% of invoices to 10%, it indicates a systemic failure in the integration (e.g., wrong prices, wrong addresses, double billing).

The "Clean Sweep" Reserve: Smart acquirers often negotiate a specific reserve in the purchase agreement for legacy disputes. This allows the integration team to quickly write off small, contentious legacy balances to "clean the slate" and focus on the new relationship, rather than spending dollars to collect cents.

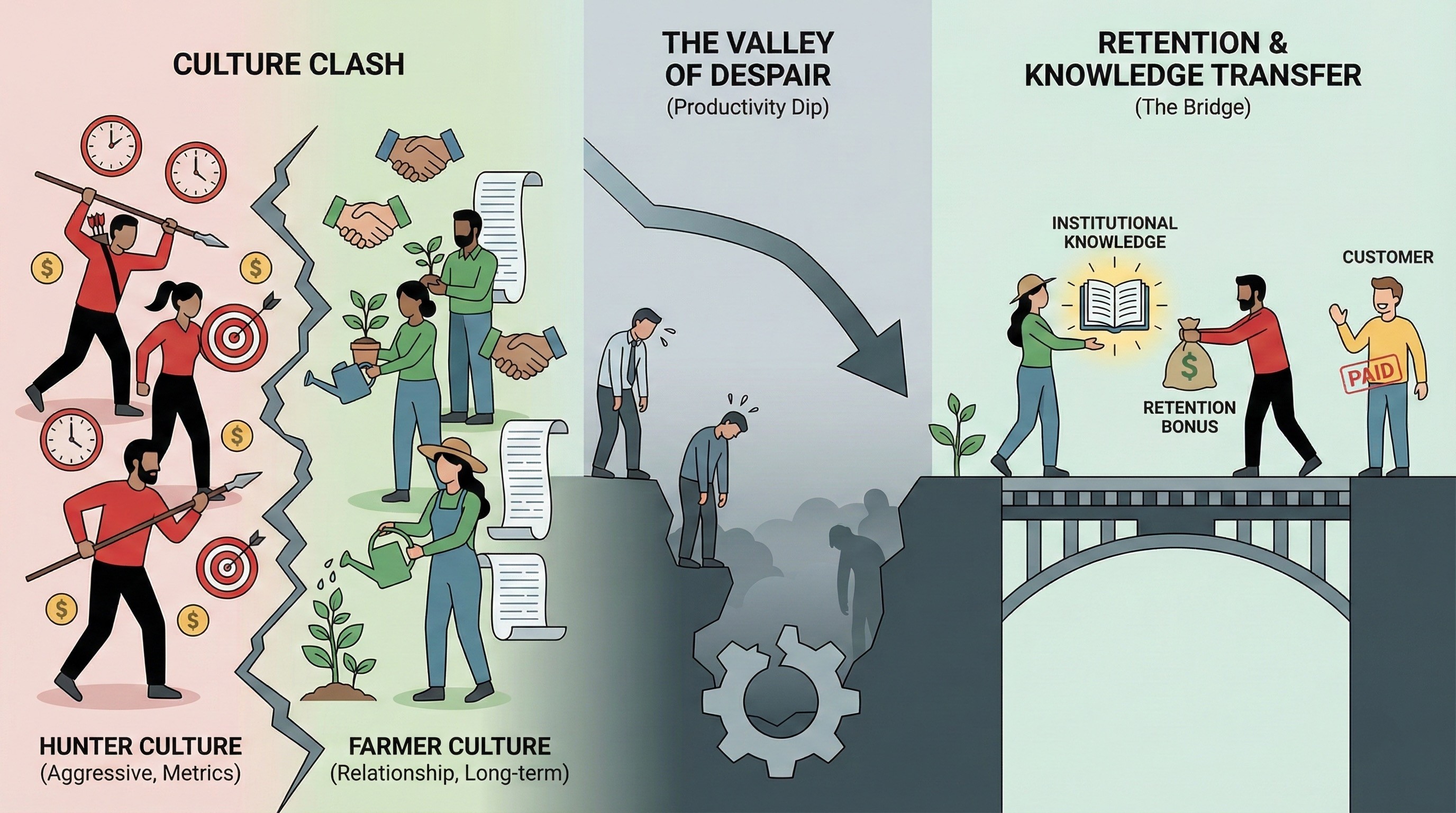

The Human Element: Culture, Retention, and Change Management

Ultimately, Accounts Receivable is a human endeavor. It relies on the relationships between collectors and accounts payable clerks. M&A disrupts these relationships.

The Culture Clash in Collections

Different companies have different "Collections Cultures."

The "Hunter" Culture: Aggressive, metrics-driven, focused on hitting monthly cash targets at all costs. Often found in PE-backed firms.

The "Farmer" Culture: Relationship-driven, lenient on terms to preserve long-term sales, often found in family-owned businesses.

The Clash: If an acquirer with a Hunter culture takes over a target with a Farmer culture and immediately imposes aggressive tactics, they risk alienating the customer base. The "Farmer" staff from the target company may also resign in protest, taking their institutional knowledge with them.

Staff Retention and the "Dip"

There is almost always a dip in productivity ("The Valley of Despair") following a merger announcement. Staff are anxious about their jobs.

Retention Bonuses: It is critical to identify the key AR staff in the target company, those who know the "story" behind the difficult accounts, and offer them retention bonuses to stay through the system migration (typically 6-12 months).

Knowledge Transfer: Before these staff leave, their knowledge must be captured. This is not just process documentation; it is the nuanced knowledge of how to get paid by specific customers (e.g., "For Customer Z, you have to email Mary, not the AP inbox, and you have to do it on Tuesdays").

The Integrated Future

The successful integration of Accounts Receivable in M&A is a microcosm of the entire deal. It requires the precision of a forensic accountant, the foresight of a strategic planner, and the empathy of a customer service leader.

The journey from the initial valuation of the asset to the final decommissioning of the legacy system is fraught with risks, ghost assets, channel stuffing, data corruption, and culture clashes. However, by adhering to a rigorous framework, utilizing Clean Rooms for diligence, enforcing strict Day 1 continuity protocols, treating data migration as a transformation rather than a lift-and-shift, and leveraging the emerging power of AI, acquirers can turn this perilous transition into a source of value.

In the final analysis, the goal is simple: ensure that when the dust settles, the cash is flowing faster, the data is cleaner, and the customers remain loyal. The invoice is the handshake of commerce; ensuring it remains firm during a merger is the first step toward a successful union.